Table of Contents

There’s something almost rebellious about the 130/30 strategy. While the rest of the investment world spends centuries perfecting the art of picking winners, someone decided the real edge might come from simultaneously betting against losers. It’s a bit like a restaurant critic who doesn’t just recommend great restaurants but actively warns you away from bad ones. The question is whether this dual approach actually helps when markets turn ugly, or if it just gives you twice as many ways to be wrong.

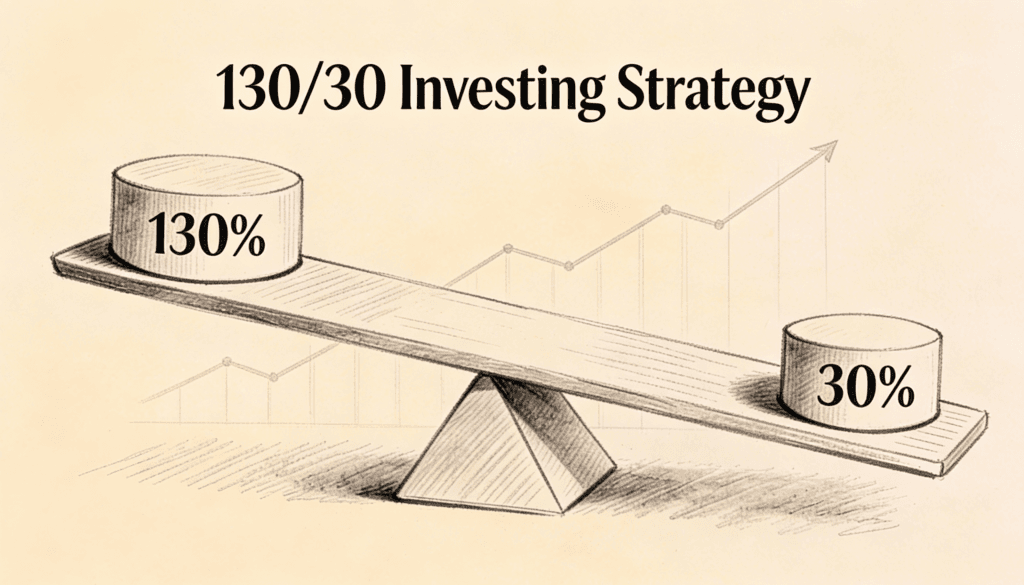

Traditional long only investing has the virtue of simplicity. You buy things you believe will go up. When they go up, you make money. When they go down, you lose money. The logic is clean, almost Newtonian in its directness. The 130/30 strategy introduces a twist: you’re still net 100% long like a traditional portfolio, but you get there by being 130% long and 30% short. You borrow stocks you think will decline, sell them, and use that money to buy more of what you think will rise.

The mathematical elegance masks a deeper philosophical question about how markets actually work when they’re falling apart. Bear markets aren’t just bull markets in reverse, running the same film backward. They’re different beasts entirely, with their own psychology, their own rhythms, their own rules.

The Architecture of Falling

Think about what happens in your mind when you watch something fall. A glass slipping from a table has a different quality than a glass rising to your lips. The fall has inevitability to it, acceleration, a sense of gravity taking over. Bull markets require fuel, constant energy input, reasons to keep climbing. Bear markets just need gravity to stop being opposed.

This asymmetry matters enormously for how different strategies perform. A long only portfolio in a bear market is fighting gravity with every position. Each stock you own is trying to swim upstream against a current that’s pulling everything down. You might have picked the best swimmers, but they’re all swimming in the wrong direction relative to where the river is going.

The 130/30 approach tries to harness some of that gravitational energy. Your short positions are working with the current, not against it. In theory, this should provide ballast, maybe even propulsion. When everything is going down, at least some of your bets benefit from that movement.

But here’s where it gets interesting. The assumption hiding in plain sight is that in a bear market, bad stocks will fall more than good stocks. This seems obvious until you examine it closely. Sometimes bear markets are surprisingly egalitarian. They take down cruise ships and dinghies with equal enthusiasm.

The Correlation Trap

Financial markets have this peculiar quality where diversification works brilliantly until the exact moment you need it most. It’s like an umbrella that functions perfectly in light drizzle but collapses in a hurricane. During calm times, stocks move somewhat independently based on their individual merits. During crashes, they often move together, pulled by the same fear that overrides company specific considerations.

This creates a paradox for the 130/30 strategy. Your longs and shorts are meant to cancel out some systemic risk, leaving you exposed mainly to the difference in quality between your good picks and bad picks. But if correlations spike toward one during a crisis, that quality difference can shrink dramatically. Everyone’s moving together, just at slightly different speeds.

The traditional long only investor, oddly enough, doesn’t face quite this same dilemma. They’re fully exposed to systemic risk, yes, but they’re not caught in the squeeze between converging correlations. They’re not betting on spreads that can compress. They’re simply betting on direction, and in a bear market, they’re simply wrong, with clarity.

There’s something almost cleaner about being straightforwardly wrong than being wrong in a complex way. The long only portfolio’s losses in a bear market are disappointing but unsurprising. The 130/30 portfolio’s losses, if they occur, feel like a betrayal of sophistication. You did something more clever, and it didn’t help.

The Leverage Question Nobody Wants to Discuss

Here’s an uncomfortable truth: the 130/30 strategy involves leverage. You’re getting 160% gross exposure from 100% capital. That leverage is relatively modest compared to hedge fund cowboys running around with 10x leverage, but it’s leverage nonetheless.

Leverage in normal times is like a tailwind. It amplifies your edge. Leverage in crisis times is more like a straitjacket worn while trying to swim. The problem isn’t just that you can lose more. The problem is that leverage requires margin, and margin can be called at the worst possible moments.

Imagine you’re running a 130/30 portfolio and the market drops 20%. Your longs are down, your shorts might be helping somewhat, but your broker is looking at your account and seeing diminished collateral. They want more money or they want you to close positions. Closing positions in a panicked market means crystallizing losses at terrible prices.

The traditional long only investor faces portfolio losses but typically doesn’t face forced selling beyond their own panic threshold. They can hold through the storm if they have the stomach for it. The 130/30 investor might not have that choice. The mechanics of the strategy can force actions that a long term holder would never voluntarily take.

When Shorts Stop Working

There’s a fascinating dynamic in bear markets where short positions can actually start to work against you in unexpected ways. It sounds counterintuitive. Stocks are falling, you’re short stocks, shouldn’t you be celebrating?

The issue is short covering. When many investors are short the same stocks, and those stocks fall significantly, there’s an overwhelming temptation to take profits. Everyone tries to buy back their shorts at once, creating sudden, violent upward price spikes in the middle of an overall downtrend. These squeezes can be brutal.

Additionally, regulatory environments can turn hostile. History is littered with moments where authorities, faced with market chaos, temporarily ban short selling. Suddenly your carefully constructed 130/30 portfolio is just 130 long with no hedge. You’ve built a machine designed for balance, and someone removed one side of the mechanism.

The traditional long only portfolio, in contrast, is never fighting its own design. It’s designed to go up when markets go up and down when markets go down. There’s no mechanism that can jam or regulatory intervention that can break the strategy’s fundamental logic.

The Psychology of Double Jeopardy

Managing a 130/30 portfolio requires you to be right in two different ways simultaneously. You need to identify stocks that will outperform and stocks that will underperform. In bull markets, this dual challenge is exciting. In bear markets, it’s exhausting.

When markets are falling, every decision carries the weight of double scrutiny. Did you short the right stocks? Are they falling faster than your longs? Are you sure the stocks you’re long in are really the highest quality, or are they just expensive stocks that will fall later and harder? The mental overhead multiplies.

Long only investors face despair in bear markets, but it’s a simpler despair. They watch their portfolio fall and wonder when it will stop. The 130/30 investor watches their portfolio fall and wonders whether it’s falling less than it should be given the strategy’s design, whether the shorts are pulling their weight, whether they should adjust the positions, whether the whole apparatus is still functioning as intended.

There’s research from psychology showing that cognitive load impairs decision making. When you’re tracking more variables, making more decisions, watching more positions move in more directions, you’re more likely to make mistakes. Bear markets already impair judgment through fear and uncertainty. Adding strategic complexity on top might not be the gift it appears to be.

The Survivor’s Paradox

Here’s something worth considering: most backtests and performance comparisons of 130/30 versus long only strategies come from a world where both strategies survived to be analyzed. The portfolios that blew up, that faced margin calls they couldn’t meet, that got caught in regulatory changes or liquidity crunches, those don’t show up in the tidy comparison charts.

This survival bias might favor simpler strategies during extreme times. Long only portfolios can suffer tremendously and still exist on the other side of a bear market. They might be down 40% or 50%, but unless the investor panic sold everything, the positions remain. The strategy can recover when markets recover.

Leveraged strategies have failure modes that don’t allow for comeback stories. You can be right about long term direction but still get wiped out by short term margin dynamics. The 130/30 strategy, with its relative modesty in leverage terms, is less vulnerable than truly wild hedge fund strategies, but it’s more vulnerable than plain long only investing.

What Bear Markets Actually Reveal

Perhaps the deepest insight isn’t about which strategy wins in bear markets but what bear markets reveal about investing itself. They expose that most strategies are optimized for normal times, not exceptional times. The 130/30 approach is brilliant in a market with reasonable dispersion, where skill in stock picking matters and can be expressed through both long and short positions.

Bear markets can collapse dispersion. They can make skill less relevant than positioning. They can turn elegant strategies into clumsy ones through no fault of the strategist. In this light, the traditional long only approach has an accidental virtue: it’s already so simple that there’s little complexity to break down under stress.

This doesn’t mean long only is better. It means it’s more robust in the specific sense that it fails in predictable ways. When the market falls 30%, your long only portfolio probably falls close to 30%, maybe a bit less if you picked good stocks. When the market falls 30% and you’re running 130/30, the outcome depends on a longer chain of causation: how much your longs fell, how much your shorts fell, what happened to correlations, whether you faced margin issues, how dispersion evolved.

Longer chains of causation create more opportunities for unexpected outcomes. Sometimes those outcomes are surprisingly good. More often in bear markets, they’re surprisingly bad in ways that are hard to anticipate.

The Uncomfortable Conclusion

If you forced a choice for bear market performance, the answer frustrates anyone looking for sophistication to triumph. Traditional long only portfolios probably hold up better in severe bear markets, not because they’re better strategies in an absolute sense, but because they’re more failure resistant.

The 130/30 strategy is genuinely clever. It tries to harvest the full spectrum of your insights, both positive and negative. It tries to reduce systemic risk while maintaining exposure. It tries to improve efficiency. All of these are worthy goals.

But bear markets aren’t interested in your goals. They’re stress tests that find weak points in systems. The weak points in 130/30 strategies are the leverage, the correlation assumptions, the complexity of execution, and the regulatory and margin risks that come with shorting. Long only strategies have fewer weak points to exploit, mainly because they’re too simple to have many weak points.

There’s a broader lesson here about financial innovation. New strategies typically get developed and refined during good times. They get marketed based on how they improve outcomes when markets cooperate. The real test comes when markets stop cooperating, and that’s precisely when the innovations often reveal they were optimized for the wrong scenario.

This doesn’t mean you should never use 130/30 strategies. It means you should know what you’re buying. You’re trading some potential bear market resilience for better expected performance in normal markets. That might be a trade worth making, especially if bear markets are rare and you have a long time horizon.

But if someone promises you that a more sophisticated strategy will protect you better when everything falls apart, you should be skeptical. Sometimes the old, simple ways persist not because people are too dumb to adopt better approaches, but because simplicity itself has value that only becomes apparent when complexity becomes a liability.

The bear doesn’t care how clever your strategy is. It might even prefer clever prey.

At least they’re more interesting to take apart.