Table of Contents

The Most Expensive Misunderstanding in Income Investing

There is a particular kind of investor who speaks about dividends the way medieval peasants once spoke about the king’s grain. With reverence. With gratitude. As though the cash that appears in a brokerage account every quarter is a gift, a bonus, a little something extra layered on top of whatever the stock itself happens to do. This belief is one of the most expensive misunderstandings in all of personal finance, and once you start looking for it, you will notice it everywhere.

Understanding how dividends actually work requires setting aside the comforting story and looking at the plain accounting reality underneath it. The reality is simpler, colder, and far more useful than the folklore. The problem is not that dividends are bad. Dividends are perfectly fine. The problem is that millions of people have convinced themselves that dividends are something they are not, and that belief quietly shapes their portfolios, their tax bills, and ultimately their lifetime wealth in ways they never bother to look up.

The dividend illusion hides inside YouTube thumbnails promising passive income. It animates entire online communities. It powers a small industry of newsletters, exchange traded funds, and books built around the seductive idea that you can simply collect checks forever and never touch the principal. Let us walk through why so much of that framing is misleading, and what a clearer understanding can do for your money.

The Magic Trick That Is Not Magic

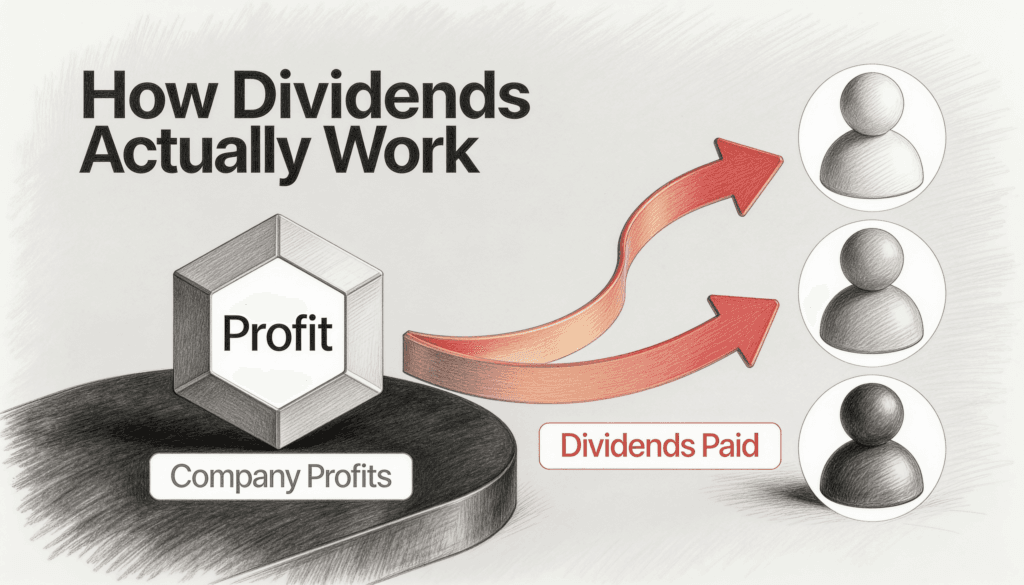

Imagine you own a small bakery. The bakery is worth one hundred thousand dollars. One day you decide to take five thousand dollars out of the till and put it into your personal pocket. Are you richer than you were that morning? Of course not. You now hold five thousand dollars in cash and a bakery worth ninety five thousand dollars. The total is unchanged. You simply moved money from one pocket, the business, into another pocket, yourself.

A dividend works in exactly this way. When a company pays you one dollar per share, that dollar has to come from somewhere. It comes out of the company’s cash reserves. The company is now worth one dollar per share less than it was the day before. This is not a theory or an opinion or a matter of investing philosophy. It is mechanical. Stock exchanges actually mark the share price down on the ex dividend date to reflect precisely this adjustment.

A dividend does not add wealth to your account. It transfers value that already belonged to you from inside the company into your hand, and the market adjusts the price of what remains to match.

The market is not confused about what happened here. Only the investor tends to be. And yet the language we use around dividends pretends otherwise. We say things like “the stock paid me.” We talk about “income.” We speak as though the dividend materialized from nowhere, like a tip from a generous universe. But you did not get paid in the way that word implies. You received a portion of your own equity in cash, and the market adjusted the value of everything you still hold accordingly.

This is the heart of the misunderstanding. People treat dividends as additive when, in the strictest accounting sense, they are a transfer. The cash did not appear. It relocated with a backpack made of cash with cash inside of it.

Why the Numbers Are Not Up for Debate

If you owned every single share of a company and that company paid out a one dollar per share dividend, you would simply be moving your own money from the corporate bank account into your personal one. Nothing about your net worth would change. The same principle holds when you own one share out of millions. Your slice of the pie is identical the day after the payment. The pie is just slightly smaller, and you are holding a small piece of it as loose cash.

Why the Illusion Is So Sticky

If the mathematics is this clean, why do so many otherwise intelligent people get it wrong? The answer is that human beings did not evolve to think in spreadsheets. We evolved to think in stories, and the dividend story is a genuinely beautiful one.

It feels like ownership made tangible. It feels like the company is acknowledging you personally, mailing you a small envelope of thanks every quarter. It feels like the sort of thing a wise grandfather would have done, back when men wore hats and a stock certificate was a physical object you could hold in your hands. There is real emotional weight in that, and emotional weight does not respond well to accounting logic.

There is also a deep psychological comfort in receiving cash that you did not have to ask for. Behavioral economists have a precise name for what is happening here. They call it mental accounting. We sort money into different mental buckets and treat those buckets differently even when they are economically identical.

A dollar earned from selling a share feels like eating your seed corn. A dollar received as a dividend feels like a harvest. It is the same dollar. The only difference is the story you tell yourself about where it came from.

This is not a small or harmless bias. It is the entire emotional foundation of the dividend industry. Companies understand it. Fund managers understand it. They have built marketing campaigns around the emotional gap between two outcomes that, on a balance sheet, are exactly the same. The feeling of being paid is the product. The accounting reality is the fine print that almost nobody reads.

The Tax Bill You Did Not Need to Pay

Here is the point where the illusion stops being merely philosophical and starts becoming financially expensive in dollars you can count. When a company pays you a dividend, in most jurisdictions you owe tax on that payment. Right now. This tax year. Whether you wanted the cash or not. The company decided on your behalf, and the tax authority is more than happy to collect its share.

Now contrast this with the alternative. Suppose the company had simply kept that cash and reinvested it into the business, or used it to repurchase its own shares. The share price would reflect that retained value. You would still own exactly the same percentage of the company. But you would not owe a single cent in tax until the day you chose to sell, in an amount you chose, possibly years or even decades later, perhaps at a time when your personal tax situation is far more favorable.

A dividend is, in effect, a taxable event that the company imposes on you without asking permission. If you do not actually need the income to live on, you are paying taxes today on money that could otherwise have compounded untouched for another twenty or thirty years.

The Drag Compounds Quietly

Over a long enough time horizon, this tax drag is anything but trivial. It can be the difference between arriving at retirement comfortable and arriving at retirement genuinely wealthy. Every dollar paid out and taxed early is a dollar that never gets the chance to grow on top of itself in the years that follow.

Reinvesting dividends in a taxable account is the financial equivalent of taking water out of the pool, paying tax on it, and then pouring the very same water right back in.

The retiree who genuinely needs to draw income from a portfolio at least has a reason to want dividends, although even that investor could accomplish the same outcome by selling a small portion of shares periodically, with far more control over timing and amount. The thirty five year old who reinvests dividends inside a taxable account, by contrast, is paying tax every single year for the privilege of receiving their own money and immediately handing it straight back to the company that just gave it to them.

The Quality Question Most Investors Skip

There is a second, subtler problem that the income obsessed rarely consider. Dividends shape behavior at the company level too, and not always in a healthy direction.

When a company commits publicly to a dividend, it has effectively made a promise to its shareholders. Cutting that dividend is treated by the market as a confession of failure. The stock gets punished. Management gets blamed in the financial press. So companies will go to extraordinary and sometimes self destructive lengths to keep the dividend intact, even when the underlying business no longer justifies the payment.

This commitment sounds noble on the surface. In practice it can mean borrowing money simply to fund the dividend. It can mean slashing research and development budgets. It can mean delaying necessary capital investment in the core business. It can mean a slow, quiet erosion of the very company that produced the dividend in the first place, all in service of maintaining an appearance of stability for one particular type of shareholder.

A dividend is not automatically a sign of corporate strength. In some cases it is a signal that management simply could not think of anything more productive to do with the cash. A growing company with abundant high return opportunities usually wants to keep its money working inside the business. A company that mails it all out the door may be telling you, without saying so directly, that its best growth days are behind it.

The Investor as Tenant Versus the Investor as Owner

Here is a framework that may make the whole question click into place. When you focus primarily on dividends, you are behaving like a tenant. You care about the rent check. You watch the mailbox. You judge the quality of the building mainly by whether the check clears on time each month.

When you focus instead on the underlying business, you are behaving like an owner. You care about whether the building is appreciating, whether the neighborhood is improving, whether the structure itself is sound and well maintained. The rent is merely one feature of ownership rather than the entire purpose of it.

Both mindsets can be valid in the right context. The retiree drawing down a portfolio is genuinely operating in tenant mode, and that is entirely appropriate for their stage of life. But the accumulator, the person who is still actively building wealth, is frequently paying a very real cost in order to feel like a landlord when they would be far better served acting like a developer.

How the Dividend Filter Narrows Your World

The dividend mindset quietly narrows your investable universe. It excludes from consideration many of the finest businesses on the planet purely because those companies choose to reinvest their profits rather than distribute them. It rewards mature companies in slow moving industries and penalizes the younger ones that are still compounding at high rates. It is a filter that pretends to select for quality but very often selects for nothing more than age.

The dividend screen does not separate good businesses from bad ones. It separates companies that distribute cash from companies that retain it, and those two categories have very little to do with future returns.

Some of the greatest wealth creation stories of the past several decades came from companies that paid no dividend at all for years, choosing instead to plow every available dollar back into growth. An investor wedded to yield would have screened those companies out before ever giving them a look.

A Quiet Test You Can Run on Yourself

If you are not entirely sure where you stand on this, try a simple thought experiment. Suppose you own a stock that currently pays a four percent dividend. Tomorrow morning the company announces that it will stop paying dividends entirely and will instead reinvest all of that cash into the business. The market reacts with a shrug. The share price barely moves, because everyone understands that the money is still inside the company, simply deployed in a different way.

Now ask yourself honestly: how do you feel?

If your very first reaction is disappointment, irritation, or a sudden urge to sell, you have just learned something important about yourself as an investor. You were not truly invested in the business. You were invested in the check. The check was the entire point. The business was merely scenery in the background.

There is nothing shameful about this, but it is worth being honest about, because investing for the check rather than the business changes everything downstream. It changes what you buy. It changes how you define success. It changes how you react to news. And in most cases, particularly over long time horizons and inside taxable accounts, it quietly leaves real money on the table year after year.

Common Questions About How Dividends Work

People often ask whether reinvesting dividends avoids the tax problem. In a taxable account, it does not. Even when your dividends are automatically reinvested into more shares, you still owe tax on them in the year they are paid, because the tax authority treats the payment as income the moment it lands, regardless of what you do with it next.

Another frequent question is why the stock price drops on the ex dividend date. The answer is mechanical rather than mysterious. The company has parted with cash, so each share now represents a slightly smaller pool of corporate value. The exchange adjusts the opening price downward by roughly the dividend amount to reflect that the cash has left the building.

What to Actually Do With This Understanding

None of this should be read as an argument against ever owning a dividend paying stock. Many genuinely wonderful businesses pay dividends. Some of them have raised their dividends every year for decades, precisely because they generate more cash than they can productively reinvest, which is itself a meaningful sign of underlying strength.

The argument here is not against dividends themselves. It is against the framing that surrounds them. If you believe dividends are free money falling from the sky, you will chase them. You will buy companies for their headline yield rather than for the quality of their operations. You will pay taxes you never needed to pay. You will pass over superior businesses simply because they decline to mail you a quarterly thank you note. And you will feel quietly virtuous the entire time, because you are following advice that sounds prudent and old fashioned and safe.

The investor who genuinely understands what a dividend is can still own dividend paying stocks with a clear conscience. They simply own them for the right reasons. They never confuse a return of their own capital with a return on it. They do not allow a quarterly check to distract them from the far larger question of whether the business is actually growing in value over time.

A dividend is your own money being handed back to you, frequently with a tax bill attached, by a company that has decided on your behalf that it could not find a better use for the cash.

Sometimes that decision is a wise one. Sometimes it is not. Either way, treating the payment as found money is the most expensive form of gratitude there is. The wiser path is to stop thanking the mailbox and start asking what the building is actually worth.

Once you make that shift in how you think, you will find that you evaluate every company more clearly, you keep more of your money working for you, and you stop confusing the comforting feeling of being paid with the harder reality of being enriched.