Table of Contents

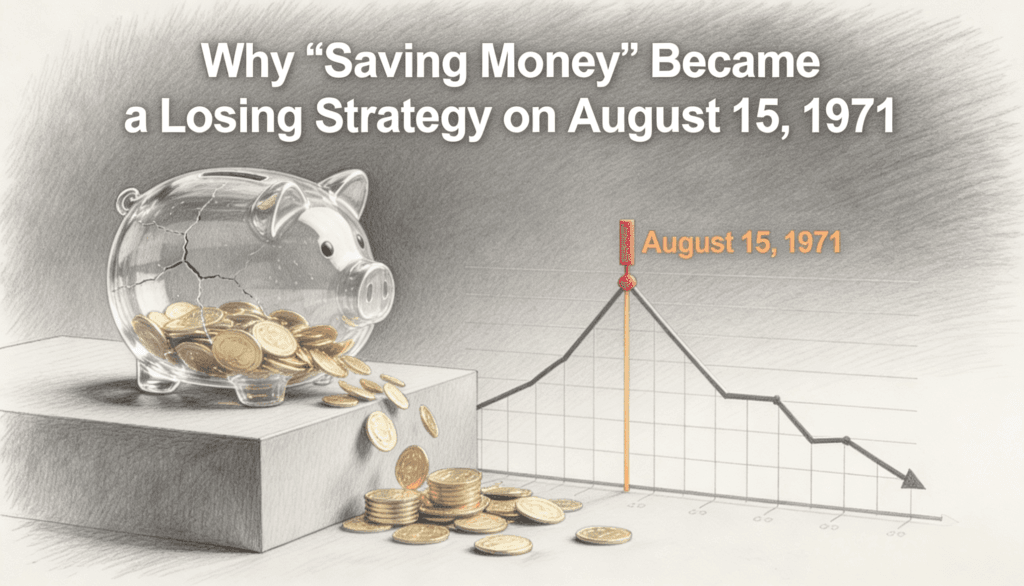

There is a date that changed everything about money. Most people have never heard of it. It was not a war. It was not a crash. It was a quiet Sunday evening announcement by a president who would later resign in disgrace. And yet, what Richard Nixon did on August 15, 1971 altered the financial lives of every person on the planet more than almost any single policy decision in modern history.

He killed the gold standard.

And with it, he killed the old logic of saving.

The World Before the Nixon Shock

To understand what broke, you have to understand what existed before. Since the end of World War II, the global monetary system ran on an agreement called Bretton Woods. The idea was simple. The US dollar was pegged to gold at $35 per ounce. Other currencies were pegged to the dollar. This meant that money was, in a very real sense, tethered to something physical. Something scarce. Something that governments could not just conjure out of thin air.

Under this system, saving money was rational. If you put a dollar in the bank in 1950, that dollar held roughly the same purchasing power a decade later. The value of your labor, stored as currency, stayed relatively intact. Your grandfather was not crazy for stuffing cash in a mattress. The system rewarded patience and discipline. You worked, you saved, and your savings meant something.

This is the world your grandparents understood. And it is the world that ended one summer night in 1971.

What Nixon Actually Did

By the late 1960s, the United States had a problem. It was fighting an expensive war in Vietnam. It was funding ambitious social programs. It was spending more than it had. Foreign governments, particularly France, started noticing that America was printing more dollars than it had gold to back them. So they did the logical thing. They started showing up and asking for their gold.

This was like a bank run, except the bank was the United States government.

Nixon had two choices. He could cut spending dramatically, which was political suicide. Or he could simply break the link between the dollar and gold, which would let the government print as much money as it wanted without anyone being able to call the bluff.

He chose the second option. He went on television, framed it as protecting America from “international money speculators,” and suspended the convertibility of dollars into gold. Temporarily, of course. The temporary suspension is now over fifty years old.

The Invisible Tax That Followed

Here is what changed in practical terms. Before 1971, the money supply was constrained. Governments could not print unlimited currency because they needed gold to back it. After 1971, that constraint vanished. Money became purely abstract. It was valuable because the government said it was valuable. Nothing more.

This unleashed something that had always existed but was previously kept on a leash: inflation. Not the dramatic, headline kind. The slow, quiet, background kind. The kind that makes a cup of coffee cost four times more over a few decades while everyone just shrugs and calls it normal.

Since 1971, the US dollar has lost over 85 percent of its purchasing power. That is not a typo. A dollar today buys a fraction of what it bought when Nixon made his announcement. And this is not unique to the dollar. Every major currency on Earth followed the same path because every major currency is now a fiat currency, backed by nothing but trust and the taxing power of its government.

Saving cash after 1971 became the equivalent of storing ice cubes in a warm room. You could do it. But you should not be surprised when you come back and find less than what you started with.

The Great Deception of Financial Advice

This is where the story gets interesting, because the cultural advice never caught up to the structural change.

For decades after 1971, parents kept telling their children to save money. Schools kept teaching the virtue of thrift. Banks kept advertising savings accounts with interest rates that barely kept pace with inflation, and often did not. The messaging stayed rooted in a world that no longer existed.

Think about how strange this is. The rules of the game changed fundamentally, but nobody updated the playbook for ordinary people. The wealthy updated theirs almost immediately. They moved into assets. Real estate. Equities. Commodities. Anything that could float upward as the currency floated downward. But the average saver kept doing what they were told. They kept storing ice cubes.

This created one of the largest silent wealth transfers in history. Not through theft. Not through conspiracy. Just through a structural change that benefited those who understood it and penalized those who did not.

Why Assets Became the New Savings Account

In a fiat currency world, the game is no longer about accumulating money. It is about accumulating things that money chases.

When governments can print currency freely, they tend to do so. Especially during crises. And when more currency enters the system, it has to go somewhere. It flows into assets. Stocks go up. Real estate goes up. Even art and collectibles go up. Not necessarily because these things became more valuable in any intrinsic sense, but because the measuring stick, the currency itself, keeps shrinking.

This is the part that confuses people. When someone says their house doubled in value over twenty years, they feel wealthier. But often, the house is the same house. Same walls. Same roof. Maybe a bit older. What actually happened is that the dollars used to measure its value became worth less. The house did not go up as much as the dollar went down.

Once you see this, you cannot unsee it. Every price chart since 1971 is partially a story about the thing being measured and partially a story about the ruler getting shorter.

The Paradox of Prudence

Here is the cruel irony. The people who were most responsible with money after 1971 were often the most punished by the system. The disciplined saver who avoided debt, lived below their means, and put cash away for the future was slowly bled by inflation. Meanwhile, the person who borrowed heavily to buy a house, which felt reckless at the time, was rewarded. Their debt got cheaper in real terms as inflation eroded it, while their asset appreciated in nominal terms.

The system, in effect, began to punish prudence and reward leverage. This was not some grand conspiracy. It was simply the mechanical consequence of how fiat money works. But the moral dimension is hard to ignore. A monetary system that punishes people for being careful and rewards people for taking on debt has some uncomfortable implications for a society that claims to value responsibility.

It is a bit like a game where the rules are written in a language most players do not speak. The few who can read it play a completely different game than everyone else.

The Modern Twist

Today, we live in an era where central banks have taken the lessons of 1971 to their logical extreme. Quantitative easing, stimulus packages, and deficit spending have become standard tools. The response to every crisis, from 2008 to 2020, has been the same: create more money.

This does not mean saving is pointless. Emergency funds matter. Cash flow matters. Liquidity matters. But holding large amounts of cash as a long term wealth strategy is like running west to chase a sunset. You will never catch it, and you will exhaust yourself trying.

The distinction is between saving as a short term tactic and saving as a long term strategy. As a tactic, keeping cash reserves for emergencies is wise. As a strategy for building wealth over decades, it has been structurally broken since 1971.

What This Means for You

The point of understanding the Nixon Shock is not to become angry about it. The decision happened over fifty years ago. The world has fully reorganized around fiat currency, and there is no going back.

The point is to understand the environment you are actually operating in, not the one you were taught about. When your savings account earns two percent and inflation runs at three to five percent, you are not saving. You are losing slowly. The numbers in your account go up, which feels good. But what those numbers can buy goes down, which is what actually matters.

This does not mean everyone should rush into risky investments. It means everyone should understand that holding cash is itself a risk. It is just a risk that does not show up on any statement. There is no line item that says “lost to inflation this month.” It is the quietest way to lose money ever invented.

The Uncomfortable Truth

August 15, 1971 was the day money stopped being something you could simply collect and hold. It became something you had to actively manage, defend, and deploy just to maintain its value. The game changed from accumulation to allocation.

The people who understood this early built enormous wealth. The people who did not were left wondering why everything kept getting more expensive while their savings account balance barely moved.

The most important financial lesson of the last half century is not about any particular investment or strategy. It is about recognizing that the very nature of money changed, and that most of the conventional wisdom about saving was forged in a world that no longer exists.

Your grandparents were right to save. You are right to question whether saving alone is still enough.

That is the legacy of one quiet Sunday evening in 1971. The rules changed. The announcement was made. And most people are still playing by the old ones.