Table of Contents

There is a strange paradox in the world of income investing. Two groups of people who want the exact same thing, a steady stream of money they did not have to clock in for, have developed a deep and almost theological disagreement about how to get it. Dividend investors look at landlords and see people who voluntarily signed up for a second job. Landlords look at dividend investors and see people who handed their financial future to a stock ticker and a prayer.

Both are partially right. Which is what makes this clash so entertaining.

The Landlord Who Never Sleeps

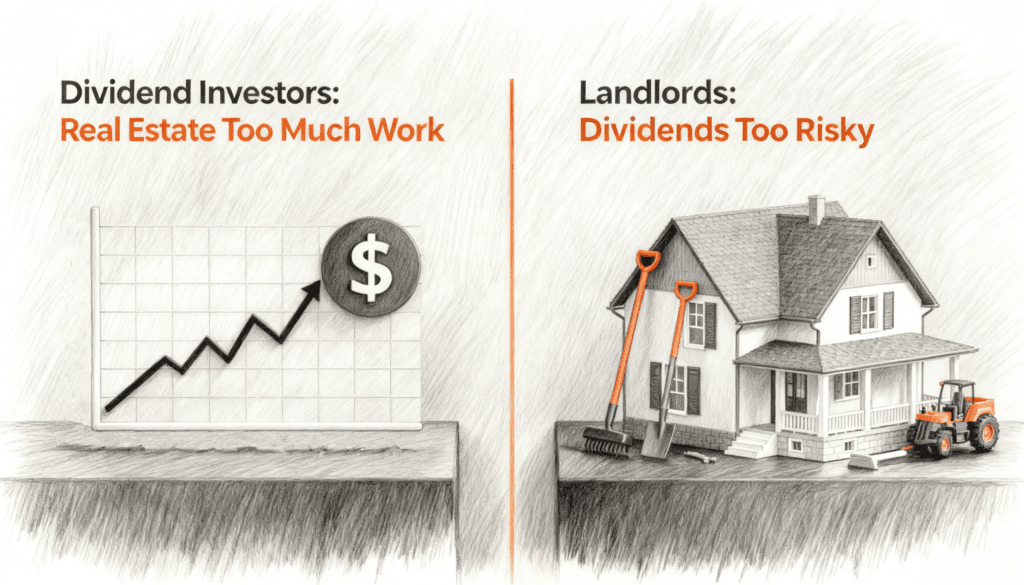

Ask a dividend investor why they do not own rental property and you will hear the same word within the first thirty seconds: work. It comes out almost like a diagnosis. Real estate, they will tell you, is not passive income. It is a small business disguised as an investment. And they are not entirely wrong.

Owning rental property means dealing with tenants, maintenance, vacancies, local regulations, property managers who may or may not be competent, and the ever present possibility that a pipe bursts on Christmas Eve. The dividend crowd sees all of this and reasonably asks: why would anyone choose this when you could buy shares of Johnson and Johnson and receive a check every quarter without ever unclogging a drain?

This is a legitimate point. But it also reveals something interesting about the dividend investor’s psychology. They are not just avoiding work. They are avoiding dependency on other people. A stock does not call you. It does not complain about the neighbor’s dog. It does not move out without notice and leave the walls looking like a crime scene. The dividend investor has built a worldview around the idea that the best investment is one that requires nothing from you except patience.

There is an almost monastic quality to it. The dividend portfolio is a garden that waters itself. You plant it, you wait, the payments grow, and you never have to negotiate with anyone about anything. For a certain type of personality, this is not just a strategy. It is a philosophy of life.

The Landlord’s Case Against the Screen

Now flip the mirror.

Ask a landlord why they do not just buy dividend stocks and you will hear a different word within the first thirty seconds: control. Real estate investors are, by nature, people who want their hands on the wheel. They do not trust a system where their wealth exists as numbers on a brokerage screen that can drop ten percent before lunch because a central banker in another country said something ambiguous.

And this is where the landlord makes a point that the dividend crowd tends to dismiss too quickly. Stocks are volatile. Not in the academic sense of standard deviation, but in the gut level sense of watching your portfolio lose a year of gains in a single week. The landlord sees this and thinks: my building is still standing. My tenants are still paying. The market had a panic attack and it changed nothing about my cash flow.

This is the core of the landlord’s confidence. Real estate feels real in a way that equities do not. You can drive past your investment. You can touch it. You can see it deteriorating and fix it before the problem becomes expensive. Try doing that with a stock. You cannot patch a dividend cut with a wrench.

The Risk Nobody Talks About

Here is where things get interesting. Both sides have a blind spot, and it is the same blind spot. They each underestimate the risks of their own strategy while overestimating the risks of the other.

The dividend investor worries about the landlord’s leaky roof but does not worry enough about dividend cuts. Companies reduce or eliminate their dividends all the time. General Electric did it. Ford did it. During the 2020 crisis, dozens of formerly reliable payers slashed their distributions overnight. When this happens, the dividend investor has no recourse. You cannot call the CEO and ask them to reconsider. You cannot negotiate. You just watch your income shrink and hope it comes back.

Meanwhile, the landlord worries about stock market crashes but does not worry enough about the illiquidity of real estate. When the market turns, selling a property is not like selling a stock. It takes months. Sometimes it takes years. And if you need to sell in a down market, you are not getting your price. The landlord who thinks they are protected from volatility is sometimes just protected from seeing the volatility. The building may have lost value. They just have not been forced to confront it yet.

This is the financial equivalent of the old joke about the man who falls from a skyscraper and says, as he passes each floor, “so far so good.” The absence of a daily price quote is not the same as the absence of risk. It is just the absence of information.

The Identity Problem

Beneath the spreadsheets and the cap rate calculations and the dividend yield comparisons, there is something else going on. Something that neither side would readily admit.

Choosing between dividends and real estate is, for many people, an identity decision. It is not just about returns. It is about what kind of person you want to be.

The dividend investor is often someone who values simplicity, autonomy, and intellectual elegance. They like systems. They like optimization. They like the idea that a well constructed portfolio can run on autopilot while they read books or travel or do whatever it is that financially independent people do. There is a reason the dividend community overlaps heavily with the FIRE movement. Both are built around the fantasy of escaping not just financial dependence, but dependence on other people entirely.

The landlord is often someone who values agency, tangibility, and the feeling of building something. They do not mind complexity because complexity is where they find their edge. They like the idea that their success is not determined by algorithms or analysts or market sentiment, but by their own ability to find a good deal, manage a property, and create value where others see headaches. There is a reason the real estate community overlaps with entrepreneurship. Both require a tolerance for messiness that the dividend investor finds allergic.

This is similar to what you see in the debate between people who cook at home and people who invest in restaurant stocks. One group wants to be in the kitchen. The other wants to own a piece of the kitchen from a comfortable distance. Neither approach is wrong. But you will never convince a chef that owning Darden Restaurants stock is the same as running a restaurant. And you will never convince an investor that running a restaurant is a good use of their time.

The Convergence Nobody Notices

Here is the part that should make both sides uncomfortable. The two strategies are becoming more alike every year.

REITs, Real Estate Investment Trusts, allow dividend investors to own real estate without ever touching a property. And professional property management companies allow landlords to own real estate without ever touching a tenant. The dividend investor can now collect rent through their brokerage. The landlord can now be as passive as the dividend crowd always claimed to be.

So the question is no longer really about real estate versus stocks. It is about how much distance you want between yourself and the source of your income. And that is a question that has less to do with finance and more to do with temperament.

The irony is thick. Dividend investors who own REITs are, technically, landlords. They just do not know the addresses of their buildings. And landlords who hire property managers are, functionally, passive investors. They just pay higher fees for the privilege of calling it something different.

The Real Answer

The honest truth that neither community wants to hear is that the best strategy depends almost entirely on who you are, not on what the numbers say.

If you are the kind of person who would check your portfolio every morning and panic at a red number, real estate might genuinely be better for you. Not because the returns are superior, but because the absence of a daily price quote will prevent you from making emotional decisions that destroy wealth.

If you are the kind of person who would lose sleep over a vacant unit or a difficult tenant, dividends might be better for you. Not because they are safer, but because the simplicity will prevent you from burning out and abandoning the strategy entirely.

The greatest threat to any long term investment plan is not the wrong asset class. It is the investor quitting. And people quit when the process makes them miserable. A landlord who hates being a landlord will eventually sell at the wrong time. A dividend investor who cannot stomach volatility will eventually sell at the bottom. Both end up in the same place: back at work, wondering what went wrong.

The answer was never the spreadsheet. It was the mirror.