Table of Contents

There is a quiet insult buried in the word average. Nobody dreams of being average. No child raises a hand in class and says they want to grow up to be ordinary. The word carries the weight of mediocrity, of settling, of giving up on something better.

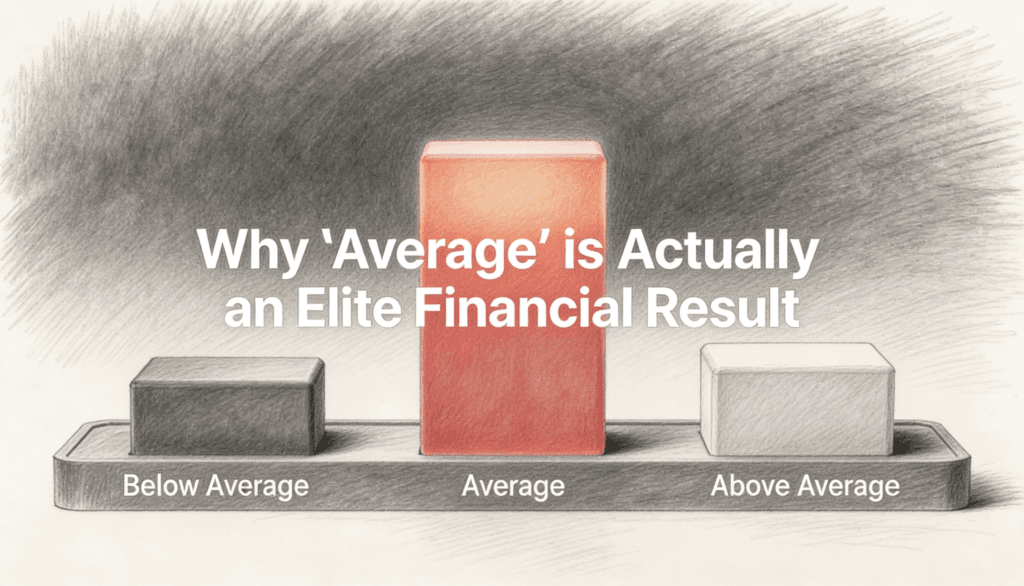

And yet in investing, average is where fortunes are built.

This is not a motivational reframe. It is not a feel good spin on laziness. It is a mathematical and philosophical reality that most people never accept because it conflicts with everything they have been taught about effort, skill, and reward.

The market’s long term average return sits somewhere around 10% per year before inflation. That number looks boring on paper. It does not make for exciting dinner party conversation. But compounded over decades, it turns modest savings into generational wealth. The people who actually capture that average, year after year, end up richer than the vast majority of those who spent their careers trying to beat it.

This is the central paradox of investing. The ambitious strategy almost always loses to the boring one.

The Effort Trap

We live in a culture that worships effort. Work harder, stay later, grind more. In most domains, this formula works reasonably well. A surgeon who practices more becomes more skilled. A writer who writes every day gets sharper. An athlete who trains with discipline gains an edge.

Investing breaks this pattern completely.

More effort in the market does not mean more return. In many cases, it means less. The investor who checks prices hourly, reads every analyst report, and adjusts their portfolio weekly is statistically more likely to underperform than someone who buys a broad index fund and never looks at it again. This is not an opinion. The data has been consistent for decades.

It is a strange thing to accept. We are wired to believe that action produces results. That doing nothing is the same as falling behind. In investing, doing nothing is often the most sophisticated strategy available. It just does not feel sophisticated, which is exactly why most people cannot stick with it.

Think about chess for a moment. Grandmasters do not move pieces constantly. Some of the most powerful positions in chess involve waiting, holding tension, refusing to act until the moment demands it. The amateur moves too often because stillness feels like surrender. The master knows that restraint is its own form of aggression.

Investing rewards the same discipline.

Why Most People Cannot Accept the Average

When your neighbor tells you about the stock that doubled in three months, something shifts inside you. Your rational brain knows that one winning trade means nothing. But your emotional brain starts whispering that you are falling behind. That everyone else has a secret you do not. That being patient is just a polite word for being left out.

This is where the damage happens. Not in the math, but in the psychology. The investor abandons their boring, reliable strategy and starts chasing the exciting one. They buy what has already gone up. They sell what has temporarily gone down. They trade their long term advantage for the short term feeling of doing something.

The financial industry understands this perfectly. It does not sell returns. It sells the feeling of being special. Every new fund, every proprietary algorithm, every exclusive strategy is marketed as your edge over the crowd. The implication is always the same: average is for people who do not know better.

But the crowd trying to beat the average is the reason the average is so hard to beat. Every active dollar traded is competing against other active dollars. For someone to win, someone else must lose. After fees, after taxes, after the friction of constant trading, most participants in that game end up behind the simple benchmark they were trying to outperform.

You are essentially paying for the privilege of doing worse.

Risk is Not What You Think It Is

Most people define risk as the chance of losing money. This definition is intuitive but incomplete. In the philosophy of investing, risk operates on at least two levels that rarely get discussed together.

The first is visible risk. This is volatility. Prices going up and down. Red numbers on a screen. This is the risk people fixate on because it is loud and immediate. It triggers fear, which triggers action, which usually triggers mistakes.

The second is invisible risk. This is the slow erosion of purchasing power. The quiet decay of money sitting in a savings account earning less than inflation. The opportunity cost of waiting for the perfect moment that never arrives. This risk makes no noise. It sends no alerts. It just compounds in silence, year after year, until the damage is done.

Here is the irony. People avoid visible risk to feel safe, and in doing so, they guarantee invisible risk. The investor who keeps everything in cash because the market feels scary is not avoiding risk. They are choosing the version of risk that does not keep them up at night. But it is still eating their future.

Accepting average market returns means accepting visible risk. It means watching your portfolio drop 20% or 30% in a bad year and doing absolutely nothing about it. This requires a kind of philosophical composure that goes against every survival instinct you have. Your brain evolved to run from danger. Sitting still while your net worth declines feels genuinely unnatural.

But the people who manage it are the ones who capture the full long term return. They earn the average by enduring what the average demands.

The Survivorship Problem

There is another layer to this that makes the average even more elite than it appears.

When people talk about investors who beat the market, they are almost always talking about the survivors. The ones who got lucky, who made the right call at the right time, who happened to be in the right sector during the right decade. The stories about the ones who tried the same thing and failed quietly are never told because failed strategies do not get magazine covers.

This is survivorship bias, and it distorts our entire understanding of what is possible.

For every investor who concentrated their portfolio into a single stock that multiplied tenfold, there are dozens who did the same thing and lost most of their money. You only hear about the winner. The losers do not write books. They do not give talks. They just disappear from the data.

When you strip away survivorship bias, the achievement of simply matching the market over a full investing lifetime is remarkable. It means you did not blow up. You did not panic at the bottom. You did not chase the wrong trend at the wrong time. You did not let a single bad decision destroy decades of good ones.

In a game where the majority of participants sabotage themselves eventually, not sabotaging yourself is an extraordinary accomplishment.

The Paradox of Enough

There is a deeper question hiding behind all of this. If average returns can build real wealth, why does almost nobody accept them?

The answer has nothing to do with finance. It has to do with identity.

We do not just want money. We want the story that comes with it. We want to be the person who saw what others missed. Who made the bold call. Who had the insight, the timing, the nerve. Accepting average returns means giving up that narrative. It means admitting that your investment skill does not matter. That the market will do what it will do, and your job is simply to show up and not interfere.

For people who have built their self worth around being competent, knowledgeable, and in control, this is genuinely difficult. It is not a financial challenge. It is an existential one.

The willingness to accept that you do not need to optimize every decision, that good enough over a long time horizon beats perfect over a short one, that the elegant move is sometimes no move at all.

But this kind of acceptance requires a maturity that the financial industry has no incentive to teach you. Contentment is bad for business. If you are satisfied with average, you do not need a financial advisor. You do not need a premium subscription. You do not need the new product, the new strategy, the new idea.

You just need time and the nerve to do nothing.

The Real Scoreboard

If we measured investing skill by consistency rather than peak performance, the rankings would look completely different. The flashy trader who made 40% one year and lost 30% the next would rank below the person who quietly earned 9% every year for three decades. But we do not measure it that way because consistency is not exciting. It does not generate clicks. It does not sell anything.

This is the final trick the financial world plays on you. It defines success in a way that makes the actual winners look boring and the actual losers look interesting. The person who went all in on a single stock and won gets a profile. The person who dollar cost averaged into an index fund for 30 years gets nothing, except the money.

There is something almost comic about it. The strategy that works best is the one nobody wants to brag about. The result that produces the most wealth is the one that sounds the least impressive at a party. The approach that requires the most discipline is the one that looks like it requires none.

Average is not what you settle for when you cannot do better. Average is what you earn when you are wise enough to stop trying to do better at a game that punishes the attempt.

That is not settling. That is winning in disguise.