Table of Contents

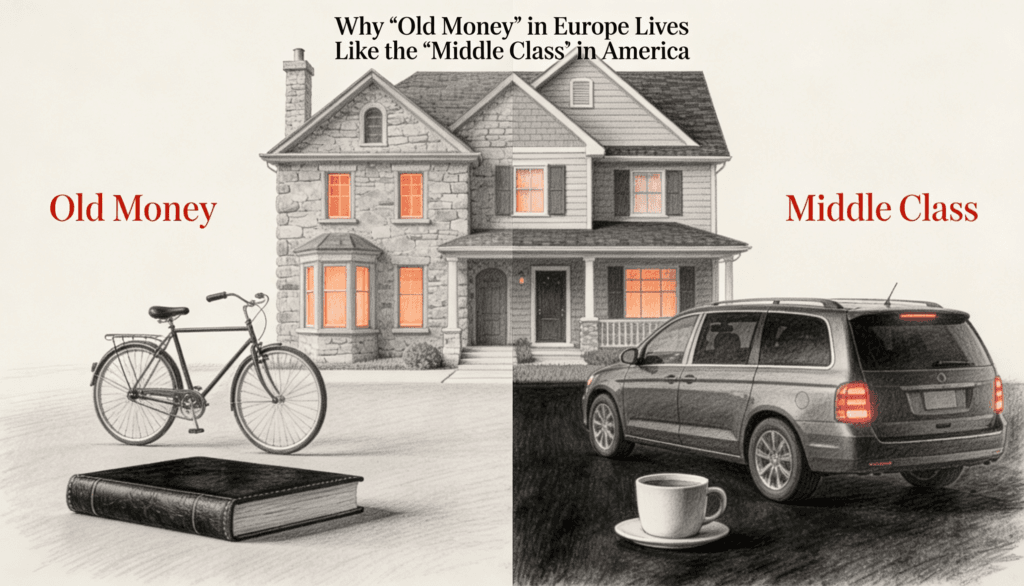

There is a strange paradox hiding in plain sight across the Atlantic. A family worth $50 million in Milan drives a Volkswagen. A family earning $120,000 in Dallas drives a BMW. One of them is rich. The other one looks rich. And that difference tells you more about wealth than any finance textbook ever will.

This is not a story about who has more money. It is a story about what money means in two places that supposedly share the same Western values. Spoiler: they do not.

The Uniform of Wealth vs. The Billboard of Income

Walk through the affluent neighborhoods of Amsterdam, Munich, or Lyon. You will notice something unsettling if you are used to American suburbs. The houses are understated. The cars are practical. The clothes are well made but not screaming any brand name at you. These people are not poor. Many of them are sitting on generational wealth that predates the United States as a country.

Now drive through an upper middle class suburb outside of Atlanta or Phoenix. The houses are enormous. The cars are leased. The kitchens have been renovated twice in ten years. Everything is designed to communicate one message: we have arrived.

The European old money family and the American middle class family might spend similar amounts in a given month. But one is spending from a well that took centuries to fill. The other is often spending from next month’s paycheck. Same restaurant, radically different balance sheets.

This is the core tension. In much of Europe, wealth is something you protect. In much of America, wealth is something you perform.

Where This Difference Comes From

You cannot understand spending culture without understanding what shaped it. Europe’s wealthy families have lived through things that American families have mostly read about. World wars fought on their own soil. Hyperinflation that turned millionaires into beggars overnight. Revolutions that seized estates. Currency collapses. Political regimes that specifically targeted the rich.

When your great grandfather watched his neighbor’s mansion get confiscated by the state, you develop a very specific relationship with visible wealth. You learn to keep your head down. You learn that the tallest nail gets hammered first.

America’s relationship with money was forged in almost the opposite furnace. Expansion. Optimism. The frontier. The gold rush. The self made narrative. In America, showing your wealth is not reckless. It is proof that the system works. It is patriotic, almost. You are supposed to want the big house. That desire is the engine of the entire economy.

So Europeans learned to hide wealth as a survival strategy. Americans learned to display wealth as a social strategy. Neither is irrational. Both make perfect sense when you understand the history behind them.

The Inheritance of Behavior

Here is where it gets interesting. These patterns have outlived the conditions that created them.

Modern Europe is not seizing estates. No one is coming for the family silver in Geneva. But the behavioral code remains. Old money families in Europe still dress modestly, still drive sensible cars, still send their children to good but not flashy schools. The threat is gone, but the habit is fossilized into identity.

Meanwhile, America has not had a true frontier in over a century. The self made story is statistically harder to pull off than it was in 1950. But the spending patterns persist. The average American savings rate has hovered around 4 to 7 percent for decades. In France, around 17 percent. The French are not earning more. They are just keeping more of what they earn.

This is what behavioral economists would call cultural anchoring. Your grandparents’ habits become your parents’ habits become your habits. Not because you thought about it. Because you never questioned it.

The Social Cost of Saving in America

Let us be honest about something that personal finance writers tend to ignore. In America, living below your means comes with a social penalty.

Try driving a ten year old Honda to a client meeting in certain industries. Try telling your friends you are skipping the vacation this year because you would rather put the money into index funds. The responses you get will range from confusion to concern to quiet judgment.

America has built a social infrastructure around consumption. Your neighborhood signals your status. Your car signals your income. Your vacations signal your success. Opting out of that system does not just save you money. It costs you social capital. And social capital, in a networking driven economy, has real dollar value.

In Europe, the calculation runs differently. In many circles, conspicuous spending signals new money, which signals a lack of sophistication, which actually costs you social capital. The incentives are reversed. A wealthy family in Florence gains respect by not showing off. A wealthy family in Houston gains respect by showing up in the right car.

This is not about one culture being smarter than the other. It is about incentive structures. People respond to what their environment rewards. And these two environments reward opposite behaviors.

The Role Nobody Mentions: Taxation and Infrastructure

There is a practical layer underneath the cultural one that deserves attention.

Europeans pay significantly higher taxes. But those taxes buy things that Americans pay for out of pocket. Healthcare. University education. Public transit. Retirement support. Childcare in many countries.

This changes the math of daily life in ways that are easy to overlook. An American family earning $150,000 might spend $25,000 a year on health insurance, $15,000 on car payments because public transit is not an option, and start saving for college tuition the day their child is born. A German family earning the equivalent has most of those costs removed from the equation before they even think about spending.

So when we say Europeans “save more,” part of that story is simply that they have fewer mandatory expenses eating into their discretionary income. The European old money family is not just culturally inclined to spend less. The system around them requires less spending to maintain the same quality of life.

Americans are not worse at saving. They are playing a more expensive game.

The Psychology of Enough

Perhaps the deepest difference is philosophical. It comes down to a single question: when is enough actually enough?

In the old money European tradition, wealth is measured in duration. The goal is not to have the most. It is to still have it in a hundred years. The family estate, the land, the name. These are things that survive if you are disciplined and disappear if you are not. Spending is the enemy of continuity.

In the American tradition, wealth is measured in altitude. The goal is to go higher. Bigger house, better car, nicer neighborhood, more impressive title. There is no natural ceiling because the system is designed to keep raising it. You hit one level and the next one appears. The hedonic treadmill is not a bug. It is the operating system.

This creates a fascinating paradox. The European old money family is objectively wealthier but feels no pressure to prove it. The American middle class family is objectively less wealthy but feels enormous pressure to appear otherwise. One is playing defense. The other is playing offense. And defense, in the wealth game, tends to win over time.

This is essentially the same principle that applies in investing. Compounding works best when you do not interrupt it. The families that have stayed wealthy for generations in Europe are families that understood this not just financially but culturally. They compounded their capital by refusing to spend it on things that depreciate, including social performance.

The Counterintuitive Lesson

Here is the part that might sting a little.

The European old money approach is, in many ways, the ultimate form of financial independence. Not because these families have more money, although many do. But because they have fewer needs. Their identity is not tied to what they buy. Their social standing does not require constant financial proof. They can lose half their portfolio and still feel like themselves the next morning.

The American middle class, by contrast, has often built an identity so intertwined with consumption that any disruption feels like an existential threat. A job loss is not just a financial problem. It is an identity crisis. Because if you cannot afford the house, the car, the lifestyle, then who are you?

That is not a financial question. It is a psychological one. And it might be the most expensive question in America.

What This Means For You

This article is not an argument that you should start living like Florentine nobility. You probably do not have a 400 year old estate to protect. And the cultural pressures you face are real, not imaginary.

But there is something worth extracting from the contrast.

The wealthiest families in Europe figured out something that most personal finance advice dances around without ever saying directly: the less your identity depends on spending, the more your wealth can grow. That is it. That is the whole secret. It is not a budgeting trick. It is not an investment strategy. It is a psychological orientation toward money that either works for you or against you.

Every dollar you spend to look wealthy is a dollar that is not making you actually wealthy. The old money families of Europe understood this so deeply that it became culture. It became heritage. It became the water they swim in.

You do not need to adopt their entire worldview. But you might want to borrow their core insight: wealth is quiet.

If it is making noise, it is probably leaving.