Table of Contents

The Trade That Went Right and Still Felt Wrong

You bought low. You sold high. You walked away with a profit that should have made your past self proud. And somehow, you feel terrible about it. This is the disposition effect in action, one of the strangest corners of human psychology, where winning feels like losing and the right decision haunts you longer than any wrong one ever could.

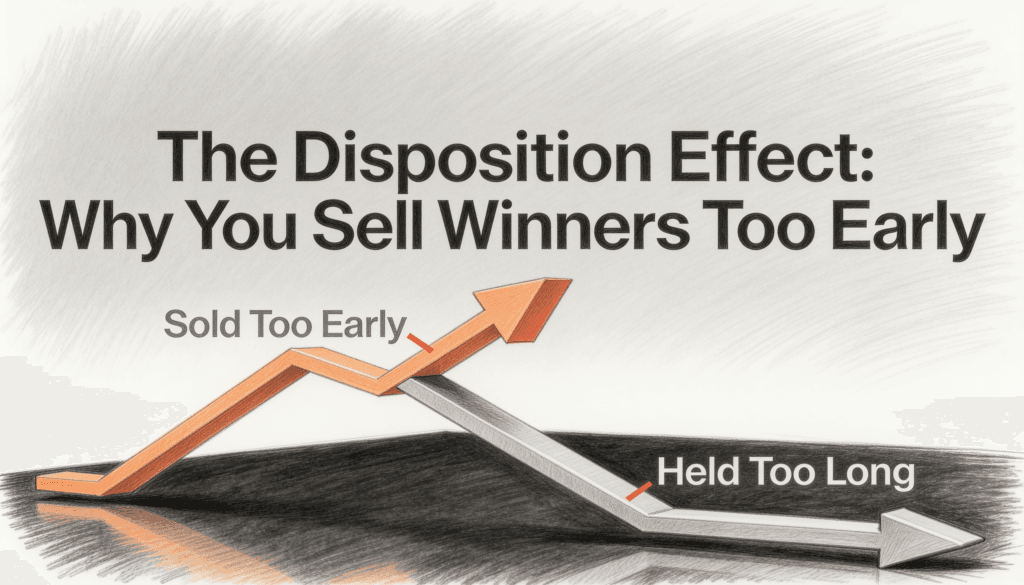

The disposition effect describes the well documented tendency of investors to sell their winners too early and hold their losers too long. It is not a rare quirk that affects only inexperienced traders. It shows up in retail accounts, in professional portfolios, and even among the people who teach this stuff for a living. Understanding why it happens, and learning to work with the way your brain actually functions, is one of the most valuable skills you can build as an investor.

Let us start with a story you have probably lived through.

The Stock That Kept Climbing After You Left

Imagine you bought a stock at $50. It climbs to $120, and you sell. A clean 140 percent return. Textbook investing. You should be celebrating.

Then the stock keeps climbing. It hits $180. Then $220. And suddenly your perfectly rational, profitable decision starts to rot in your mind like fruit left on the counter. You did not lose money. You earned money. But your brain refuses to care, because it is too busy calculating the money you could have made.

In that gap between what you earned and what you might have earned lives a very specific kind of misery that economists and psychologists call regret. And regret is not merely a feeling. It is a theory with decades of research behind it. Even the greatest minds in human history are not immune to it.

Regret Theory and the Architecture of Disappointment

In 1982, economists Graham Loomes and Robert Sugden formalized something that most investors already understood in their gut: people do not simply evaluate outcomes. They evaluate outcomes relative to what would have happened if they had chosen differently. This is regret theory, and its central insight is brutally simple.

The pain of a decision is determined not by the result itself but by the comparison between the result and the alternative you rejected.

Traditional economics assumes that people behave rationally. They weigh costs and benefits, pick the best option, and move on. Regret theory says that this picture is charming but mistaken. People carry their unchosen paths with them like luggage they can never set down. Every decision creates a ghost, a phantom version of your life where you chose differently, and you cannot stop yourself from peeking at how that ghost is doing.

When the ghost is doing better than you, it hurts. It hurts even when you are doing perfectly fine. This is the emotional engine that drives the disposition effect, and once you see it, you cannot unsee it in your own behavior.

Why Realized Gains Can Sting More Than Losses

Here is where the disposition effect gets genuinely counterintuitive. You would assume that losses generate more regret than gains. Sometimes they do. But selling a winner too early produces a flavor of regret that is almost impossible to shake, and the reason is precision.

When you sell a winner, you confront an exact counterfactual. You know precisely when you sold. You can watch exactly where the price went afterward. The comparison is not abstract. It is a number on a screen, updated in real time, mocking your decision with every upward tick.

When you lose money, by contrast, the regret stays diffuse. Maybe you should not have bought it. Maybe you should have done more research. The mistake hides somewhere in the fog of the past. But when you sell a winner too early, the regret arrives surgical. It carries a timestamp. It carries a dollar amount. It follows you home. The loss from holding a bad position feels like simple bad luck. The missed upside from selling a good one feels like a personal failure of judgment.

Selling a loser locks in a loss, which feels awful. But holding a loser preserves hope. As long as you have not sold, the loss remains theoretical. It is just paper. It might come back. The fear of selling at a loss, admitting you were wrong, and then watching the stock recover is so terrifying that many investors would rather watch their money evaporate slowly than face that possibility.

The Asymmetry Almost Nobody Talks About

There is a deeper asymmetry buried inside the disposition effect that deserves attention. When you sell and the stock drops, nobody notices. You do not call your friends to brag that you sold at the perfect time. You do not lie awake replaying the trade. The relief of avoiding a loss is real, but it stays quiet. It dissipates quickly, like steam off a cup of coffee.

When you sell and the stock rises, however, the regret turns loud and persistent. It develops its own voice. It whispers during dinner. It interrupts your weekend. Months later you are still checking the price of a stock you no longer own.

This asymmetry means the emotional ledger of selling almost always lands negative. The good outcome is barely felt. The bad outcome is felt deeply. So the expected emotional value of selling skews toward pain, even when the expected financial value points clearly toward profit.

That is why the advice to sell high feels so paradoxical. It is financially correct and psychologically brutal at the same time. The better your timing, the more exposed you become to regret. Sell at the exact peak and you will never know it. Sell a little before the peak and you will know it precisely.

The Information Curse Made the Problem Worse

Modern technology has poured gasoline on the disposition effect. In earlier decades, selling a stock meant you might glance at the price in the next day’s newspaper, maybe. The feedback loop ran slow and imprecise, which gave regret very little fuel to burn.

Today you can track every stock you have ever sold in real time, for free, on the phone in your pocket, while standing in line for coffee. The counterfactual is no longer something you have to imagine. It is something you observe continuously, in high definition. You watch the road not taken stretch out ahead of someone else who is now richer than you decided to be.

Behavioral economists sometimes call this the information curse. More information should produce better decisions. Instead it frequently produces more regret, because it makes the unchosen path vivid and specific. You are no longer wondering what might have been. You are watching what is, and it happens to be up 40 percent since you sold.

The screen that shows you a winning trade also shows you every dollar you left behind, and your brain can treat the second number as a wound if you let it.

How the Disposition Effect Shows Up in Everyday Investors

You can spot the disposition effect in some very ordinary habits. The investor who refuses to sell a stock until it returns to the price they paid is anchoring to a personal benchmark that the market does not care about. The trader who takes small, frequent profits while letting a single losing position swell into a portfolio anchor is following emotion rather than strategy. The retirement saver who cannot bring themselves to rebalance because trimming a winner feels like betrayal is paying a tax in concentration risk.

In each case the underlying mechanism is identical. Selling forces a judgment. Holding postpones it. And the human mind, given a choice between a clear verdict and an open question, will reach for the open question almost every time.

How to Manage the Disposition Effect in Practice

If regret is unavoidable, the goal becomes managing it rather than pretending you can eliminate it. Several strategies emerge from the research, and none of them require you to become smarter or more disciplined than you already are. They simply require you to be more honest about how your brain works.

Sell in Stages Instead of All at Once

If you sell half of your position and the stock keeps rising, you still have skin in the game. If it drops instead, you have locked in some profit. Partial exits do not eliminate the disposition effect, but they reduce its intensity by blurring the counterfactual. There is no single, devastating moment when you made the decision. There are several smaller moments, and the regret spreads thin across all of them.

This is one reason professional traders so often scale out of positions. They are not only managing risk. They are managing the emotional ledger that determines whether they will make a sane decision tomorrow.

Build Pre Commitment Rules Before You Buy

Decide in advance, before you ever purchase the stock, at what price or under what conditions you will sell. Write it down. When the moment arrives, execute the plan without reopening the debate. The regret will still show up, but it will be aimed at your past self’s plan rather than your present self’s judgment.

This sounds like a tiny distinction. It is enormous. Regret directed at a rule you set in a calm moment feels survivable. Regret directed at a snap decision you made under pressure feels like a referendum on your competence. Pre commitment converts a painful identity question into a simple compliance task.

Stop Watching What You No Longer Own

Once you sell, remove the ticker from your watchlist. Do not check it. The information adds nothing to your financial position, because you no longer hold the asset. It only feeds the regret machine and warps your next decision.

You might also keep a short trading journal where you record your reasoning at the moment of each sale. When regret arrives later, you can read what you actually knew and believed when you decided, rather than judging the past with information that did not exist yet. The disposition effect thrives on hindsight, and a journal starves it.

The Paradox Beneath the Paradox

There is one final layer that rarely gets discussed. Regret theory assumes the pain comes from comparing your outcome to a better alternative. But in the sell decision, there is often no alternative that avoids regret entirely. If you hold and the stock drops, you regret not selling. If you sell and the stock rises, you regret not holding. The regret is a consequence of choosing at all, not of choosing badly.

That is the real paradox underneath the disposition effect. The advice to buy low and sell high treats investing as a problem of timing. Regret theory reveals it as a problem of identity. Every sell decision becomes a statement about who you are and what you believe will happen. And because the future remains unknowable, every sell decision is also a bet that you will eventually be proven right or wrong, financially and personally.

The investors who handle the disposition effect best are not the ones who avoid regret. They are the ones who accept that regret is the price of participation.

Every trade carries an emotional cost. The goal is not to erase that cost but to stop letting it distort the next decision. The real damage of regret is not how it makes you feel about the trade you already made. It is how it makes you behave on the trade you are about to make. That is the precise moment when the disposition effect stops being philosophy and starts costing you actual money.

Putting It All Together

The disposition effect will never fully disappear, because it grows directly out of how human beings process gains, losses, and the roads they did not take. But you can shrink its influence dramatically. Scale out of positions instead of slamming the exit door. Set your rules before emotion enters the room. Close the apps that turn old trades into open wounds. Keep a record of your reasoning so your future self cannot rewrite history.

Most importantly, accept that a profitable trade you sold a little early is still a profitable trade. The phantom version of you who held for the absolute top does not exist, has never existed, and is not a fair standard for judging real decisions made with incomplete information. Once you internalize that truth, the disposition effect loses most of its grip, and you can finally let your gains feel like the wins they actually are.