Table of Contents

Why CAGR Is the Most Honest Number in Your Entire Portfolio

There is a peculiar joy in telling someone you doubled your money. The phrase carries weight, like a magic trick performed in slow motion. But the Compound Annual Growth Rate (CAGR) asks the one question that deflates the entire boast: how long did it actually take you? That single question separates real investing skill from accidental survival, and it is the reason every serious investor eventually learns to measure returns the honest way.

Doubling your money in three years is a legitimate achievement. Doubling it in eighteen years is the financial equivalent of finishing a marathon in nine hours and telling people you completed a marathon. Technically true. Deeply misleading. CAGR is the metric that takes your celebratory total return and asks, with the patience of an accountant and the quiet cruelty of a therapist, what your money actually did each year. The answer is often humbling. Sometimes it is devastating. And almost always, it reveals something true about investing that the headline numbers were designed to hide.

This article walks through what CAGR is, exactly how to calculate it, why it exposes the truth about your total returns, and how internalizing it can quietly make you a better investor than nearly everyone around you.

What Is CAGR and How Do You Calculate It

Total return is a flatterer. It tells you what you want to hear. It lets you walk around at a dinner party announcing that you are up 87 percent on a stock without anyone asking the inconvenient follow up. CAGR is the friend who asks the inconvenient follow up.

The Compound Annual Growth Rate is the single, smoothed annual rate at which an investment would have grown if it had risen at exactly that pace every single year. It takes the messy, lumpy, emotionally chaotic journey of your money and compresses it into one calm number, as if your capital had grown predictably.

The CAGR Formula

The formula is straightforward, and you only need three inputs: where you started, where you ended, and how many years passed.

- Ending Value divided by Beginning Value

- Raised to the power of 1 divided by the number of years

- Then subtract 1

Written out, it looks like this: CAGR equals (Ending Value divided by Beginning Value) raised to the power of (1 divided by Years), minus 1.

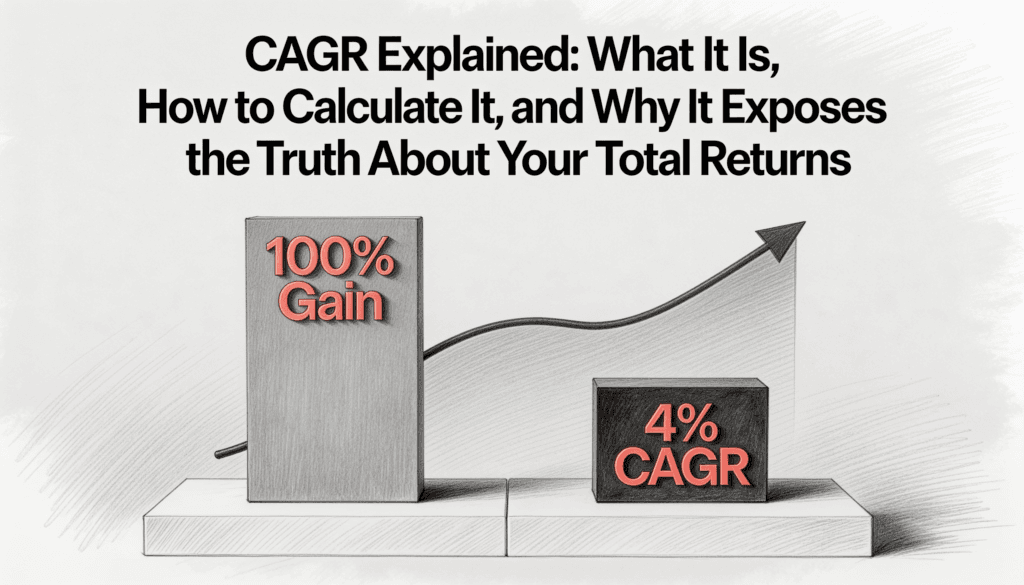

A Worked Example That Stings

Suppose you turned 10,000 dollars into 20,000 dollars over eighteen years. The total return looks glorious. You doubled. But run it through the formula. You divide 20,000 by 10,000 to get 2. You raise 2 to the power of one eighteenth. You subtract 1. The result is roughly 4 percent per year.

Four percent. That is roughly what a high yield savings account paid you during certain recent stretches, without the heartburn, without the late night chart watching, without the conviction that you were doing something clever. You were not doing something clever. You were doing something slow. And slow, when extended long enough, can dress itself in the clothing of triumph and walk right past the mirror.

CAGR strips away the drama of the journey and reveals the steady annual pace your money actually traveled. It is the difference between the story you tell and the truth the math knows.

Why CAGR Exposes the True Cost of Time

We talk endlessly about fees in investing. We talk about taxes. We obsess over expense ratios and bid ask spreads. What we rarely talk about is the most expensive resource we deploy, the one we can never recover, the one that makes everything else look trivial by comparison. Time.

When you hold an investment for ten years that returns 50 percent, you have not simply earned 50 percent. You have spent ten years of your finite life earning 50 percent. That works out to roughly 4.1 percent per year. Meanwhile, the global stock market, on its average and unremarkable autopilot, has historically delivered something in the range of 7 to 10 percent annually, depending on how you measure it and over which decades.

Opportunity Cost Hides Inside Every Total Return

This is the uncomfortable part. Investments that feel like wins on paper can be enormous opportunity costs in reality. The stock that doubled in fifteen years did not merely underperform. It actively cost you the better returns you could have earned somewhere else, while also consuming the most precious thing you own.

CAGR is not really a financial metric at all. It is a philosophical one disguised as mathematics. It is a question about how you spent your years. When you compute it honestly, you stop comparing yourself to your own beginning balance and start comparing yourself to what the patient alternative would have produced.

The Asymmetry of Loss and the Mathematics of Recovery

Here is something most people understand intellectually but refuse to feel emotionally. Losses and gains are not symmetric.

If your portfolio drops 50 percent, you do not need a 50 percent gain to break even. You need a 100 percent gain, simply to return to where you started. The downhill is gentle. The climb back is brutal.

How a Single Bad Year Can Erase a Decade

Now run that through the CAGR lens. Imagine you lose 50 percent in year one. Then over the next ten years you grind your way back to even. Eleven years have passed. Your CAGR is zero. Not low. Not modest. Zero.

In the eyes of compounding, you accomplished nothing across eleven years of your life and your capital. You ran in place on a treadmill made of your own need to be clever. This is precisely why the most successful investors are obsessed not with maximizing gains but with avoiding catastrophic losses.

The math of recovery is not the inverse of the math of decline. It is far worse. A bad year does not steal a year. It can steal a decade.

Older investors understand something the rest of us learn the hard way. Protecting capital during the worst moments matters more than capturing every percentage point during the best ones, because a single deep drawdown can quietly hollow out your long term compound rate while you are not looking.

Why Compounding Is Misunderstood by Almost Everyone

People love quoting Einstein on compound interest, usually a line he almost certainly never said, which is its own kind of poetic justice. But the worship of compounding has become so casual that the actual mechanism gets lost.

Compounding is not impressive in the short term. It is almost insulting in the short term. At 8 percent per year, your money takes about nine years just to double. Nine years. That is the span between a child being born and entering middle school. Nine years for one single doubling.

The Magic Only Lives at the Back End

The real power shows up later. The third doubling. The fourth. The fifth. This is where compounding stops being plain arithmetic and starts to look almost spiritual, where the curve bends upward so sharply it resembles a charting error rather than a real return.

But here is the catch nobody mentions at the personal finance seminars. You only reach that back end if you stay invested. And staying invested means surviving the front end, the long, boring, unrewarding stretch where compounding feels like a story told by someone trying to sell you a book.

Most people do not survive the front end. They get bored. They get scared. They get clever. They chase the asset that doubled last year, sell the one that has not moved, and quietly restart the compounding clock. Again. And again. Each restart is a small theft from their future self.

CAGR exposes the theft. It does not care about your story. It does not care that you bought low and sold high three separate times. It looks at where you started, where you ended, and how long it took. Everything in between is noise it refuses to dignify.

The Survivorship Mirage Hidden Inside Every Success Story

There is another truth CAGR helps surface, though indirectly. Most of the investment success stories you hear are the ones that survived.

The funds that blew up do not write blog posts. The traders who went broke do not host podcasts. The companies that went to zero do not get profiled in magazines. So when you hear that some fund delivered a 15 percent CAGR over twenty years, your brain registers this as proof that 15 percent CAGRs are achievable for ordinary people.

The Winners Are Loud, the Losers Are Silent

What your brain does not register is the graveyard of funds that aimed for 15 percent and delivered negative numbers, or zero, or simply ceased to exist before anyone could measure them. The CAGR you see is sampled from a distribution whose left tail has been quietly buried.

When you measure your own returns against these visible winners, you are not measuring yourself against the market. You are measuring yourself against the lottery winners while ignoring the millions of losing tickets. It is a comparison engineered to make you feel inadequate, and it is one that almost no honest financial advisor will ever encourage you to make.

The Paradox of Boring and What the Honest Investor Does

If CAGR teaches anything, it is that the boring path is frequently the most powerful one. The investor who does almost nothing, who buys a broad market index and ignores it for thirty years, will outperform the vast majority of people who constantly do something.

This is no longer a controversial claim. It is one of the most rigorously documented findings in all of finance. And yet almost nobody behaves this way.

Why Doing Nothing Feels So Hard

Doing nothing feels like wasting an opportunity. Every day brings fresh information, new tips, new fears, new temptations. The financial media exists to persuade you that this exact moment demands action. Human beings are wired to respond to stimulus, and the market produces stimulus every single second of every single day.

CAGR is the antidote to all of it. It zooms out. It compresses the noise. It says, look, here is what your activity actually produced, measured against the slow, patient alternative of doing nothing. The comparison is almost always unflattering to the activity.

The most contrarian thing you can do in modern investing is also the most boring. Choose something diversified. Hold it. Add to it. Stop looking.

How the Honest Investor Thinks

The investor who has truly internalized CAGR thinks differently. They do not get excited about a stock that has climbed 200 percent without first asking when they bought it. They do not feel poor when a friend brags about a triple without first asking how long the friend waited. They do not chase the fund manager with the spectacular three year record without first wondering what that record looks like over fifteen years.

They have developed a kind of financial attitude that comes only from doing the math honestly. They know that beating the market is hard. They know that beating it consistently across decades is nearly impossible. They know that most of their wealth, if they build any, will come from patience rather than cleverness, from refusing to sell during the long stretches when nothing seems to be working.

This is not a glamorous philosophy. It does not sell newsletters. It does not generate clicks. It is the financial equivalent of eating your vegetables and going to bed early. But it works, in the quiet way that boring things tend to work.

The Final Lesson: CAGR Is a Mirror, Not a Weapon

The most brutal truth CAGR delivers is this. Your investment results are not mostly about your intelligence. They are about your behavior, stretched across a span of time that is longer than your patience naturally permits.

Most of the difference between a great investor and a mediocre one is not analytical. It is temperamental. CAGR exposes this because it cannot be gamed. You cannot spin a better story about your returns once they are compressed into a single annual rate over a long period. The number simply is what it is. It reflects, with mathematical indifference, the cumulative effect of every decision you made and every decision you failed to make.

Ask the Inconvenient Question

So the next time someone tells you they doubled their money, ask the inconvenient question. Ask how long. Watch their face. The answer will teach you more about investing than most books ever will.

And then, quietly, ask yourself the same question about your own portfolio. The brutality is universal. It simply feels worse when it is directed inward.

That, perhaps, is the real lesson. CAGR is not a tool for judging others. It is a mirror. And like all mirrors that tell the truth, it is best approached with the understanding that what you see may not be what you hoped for, but it is almost certainly what you needed to know.