Table of Contents

There is a strange paradox at the heart of modern investing. We live in an age where information is infinite, opinions are free, and every person with a phone can trade derivatives while waiting for a burrito. Yet many investors, professional and amateur alike, lose money or barely match the market. The problem is not a shortage of knowledge. The problem is a surplus of it, combined with the dangerous belief that knowing a little about everything is the same as understanding something deeply.

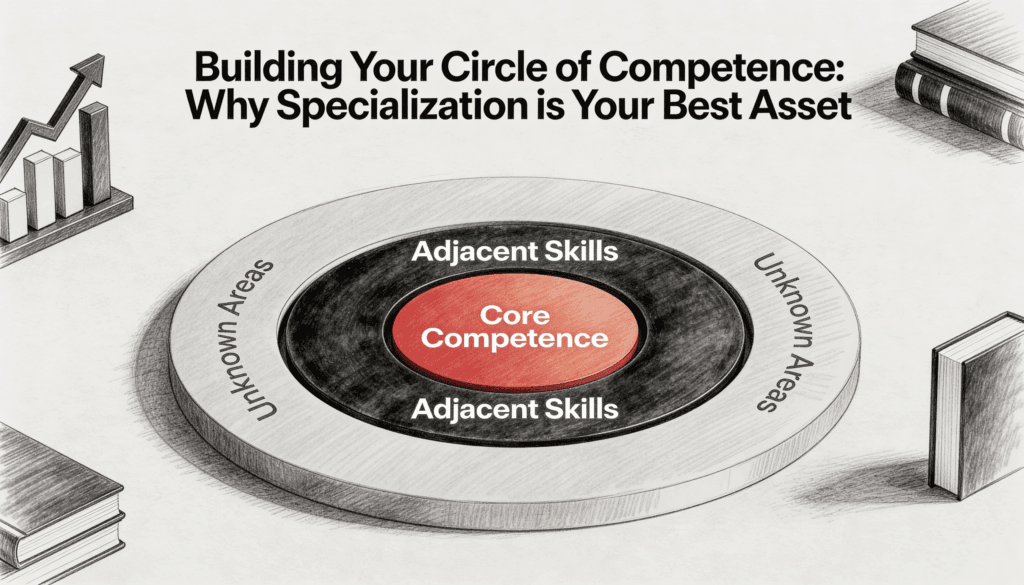

Warren Buffett and Charlie Munger gave this idea a name decades ago. They called it the circle of competence. The concept is so simple it almost sounds insulting. Know what you know. Know what you do not know. Stay inside the first circle and politely refuse to step into the second. Yet for something so obvious, it is astonishing how few people actually live by it. Most investors behave like tourists who insist on giving directions in a city they visited once during a layover.

The Tyranny of Being Interesting

Here is something the financial media will never tell you. Specialization is boring. It is boring to write about, boring to talk about at dinner parties, and boring to scroll through on social media. Nobody wants to hear that you spent six years studying the unit economics of regional waste management companies. Nobody is going to retweet your thoughtful analysis of insurance float dynamics. The algorithm rewards breadth, novelty, and confident takes on subjects you learned about yesterday.

This is the first lens through which to view the circle of competence. It is not just an investment strategy. It is a cultural rebellion. In a world that worships the generalist commentator who can discuss artificial intelligence, geopolitics, biotech, and crypto in a single podcast episode, the specialist looks almost monastic. They are the person who studies one industry the way a medieval scribe studied a single manuscript. Slowly. Repeatedly. With reverence for what they do not yet understand.

The irony is that the specialist usually wins, and the generalist usually loses money while sounding brilliant doing it. The market does not pay you for being interesting. It pays you for being right, which is a very different thing.

The Cartographer Problem

Think of investing as map making. The world of capital markets is vast, and no one has the resources to map all of it accurately. You can either draw a beautiful detailed map of one small region, or you can sketch a rough outline of the entire continent. Both feel like progress. Only one of them is useful when you are actually trying to get somewhere.

The generalist holds a map of the world with no street names. They know roughly where things are. They can tell you that energy stocks exist, that emerging markets have currencies, that biotech is risky. But when it comes time to make a decision, their map gives them nothing actionable. They are forced to rely on the maps that other people drew, which usually means listening to whoever sounded most confident on television that morning.

The specialist, by contrast, has spent years walking the same neighborhood. They know which buildings have foundation problems. They know which streets flood when it rains. They know the shopkeeper who is about to retire and the new restaurant that is quietly packing tables every night. When an opportunity appears in their territory, they recognize it instantly because they have seen it before, or something close to it, many times.

This is why a circle of competence is not really a circle. It is a depth gauge. You are not measuring how much ground you cover. You are measuring how far down you can see in one specific place.

Why Your Brain Hates Specialization

There is a psychological reason the circle of competence is so hard to maintain. The human mind was not built for it. Our ancestors who survived were the ones who could quickly assess unfamiliar situations and make decent guesses. The cautious genius who needed to study the lion for three weeks before reaching a conclusion did not pass on his genes.

This means we are wired to be overconfident in unfamiliar territory. We see a few data points, pattern match to something we vaguely remember, and feel a warm sense of certainty that has no business being there. The financial world is a perfect trap for this tendency because it offers infinite unfamiliar territory dressed up in familiar language. A balance sheet looks the same whether it belongs to a software company or a uranium miner. The numbers are formatted identically. The illusion of understanding is seamless.

A useful exercise is to ask yourself, before any investment, what specifically would have to be true for this to work. Then ask what specifically would have to be true for it to fail. If your answers sound like they came from a press release, you are outside your circle. The inside of your circle is the place where your answers are uncomfortably specific, where you can name the customers and competitors and regulatory risks without consulting Google, and where you can describe the failure modes with the same fluency as a mechanic describing why a transmission goes bad.

The Compounding Argument Nobody Makes

Most discussions of compounding focus on money. A dollar invested at a reasonable rate for forty years becomes a small fortune. This is true and well documented. What is less discussed is that knowledge compounds in exactly the same way, and possibly faster.

When you study one industry deeply for a long time, you are not just accumulating facts. You are building a mental scaffold that makes every new fact stick. The fifth year of studying that industry is more productive than the first because everything new connects to something you already understand. You start to see patterns that are invisible to people who have read three books on the subject. You can smell a bad management team from the way they answer a question on an earnings call. You can sense a turning point before the data confirms it.

This is the quiet superpower of the specialist. They are not smarter. They are not better at math. They have simply put their compounding machine in a single place and let it run for a very long time. The generalist, meanwhile, keeps starting over. They read about a new sector, get excited, lose money, and move on to the next one. Their knowledge compounds in nobody’s account.

There is a brutal kind of arithmetic here. If you spend ten years jumping between industries, you might have ten years of experience. Or you might have one year of experience repeated ten times. The difference is the depth gauge.

The Specialist as Contrarian

There is a quiet form of contrarianism in specialization that almost nobody notices. The crowd is loudest where the topics are broadest. Everyone has an opinion on the economy, on big technology stocks, on the latest macro narrative. The decibel level in these areas is deafening, and the edge available to any single investor is correspondingly small. You are competing with millions of other people who all just read the same article.

The specialist operates in quieter rooms. They study companies that nobody talks about, in industries that nobody finds glamorous, with dynamics that take years to learn. Their edge is not that they are smarter than the crowd. Their edge is that the crowd is not there. The competition has gone elsewhere to argue about something more entertaining.

This is one of the great unspoken truths of investing. The best opportunities are not where the most analysis is happening. They are where the most useful analysis is happening, which is usually a much smaller and quieter place. A specialist in a forgotten corner of the market is often facing competition from a handful of equally obscure specialists, while a generalist studying a popular stock is facing competition from millions of people, many of whom have far more resources.

How to Actually Build the Thing

Building a circle of competence is less about strategy than it is about patience and honest self assessment. It starts with picking something that genuinely interests you, because you will need years of attention and boredom is the enemy of attention. It does not have to be glamorous. The best circles are often built around industries the investor stumbled into through ordinary life. A doctor who specializes in medical device companies. A truck driver who specializes in logistics businesses. A teacher who specializes in education technology. The advantage is real because the daily experience provides a constant flow of qualitative information that nobody else has.

Then you read. Not the news, which is mostly noise, but the long material that takes effort. Annual reports going back ten or twenty years. Industry trade publications that nobody outside the industry has heard of. Books written by people who actually built companies in the field. You listen to earnings calls until the language stops feeling foreign. You build a mental library of every major event in the industry, every boom and bust, every fraud and every recovery.

This takes years. There is no shortcut, and anyone selling one is selling something else. But the payoff is something close to permanent. A circle built carefully over a decade is a circle that keeps paying you for the rest of your investing life. The companies change, the cycles repeat, and your understanding compounds in the background while everyone else is chasing the next thing.

Almost every investing mistake of consequence comes from someone stepping outside their circle while convinced they were still inside it. The crash they did not see coming, the company they did not understand, the manager they trusted because the conference room was nice. All of it traces back to the same root.

Specialization is your best asset because it is the only asset that protects you from yourself. It is the discipline of saying no to ninety nine opportunities so that you can say yes to the one you actually understand. In a world that rewards confident takes on everything, the investor who quietly knows the limits of their knowledge has a structural advantage that no algorithm and no platform can take away.