Table of Contents

There is a particular kind of horror that dividend investors feel when they watch someone day trade. It is not the horror of watching money being lost. They can live with that. Losses happen. Markets fall. Mistakes are part of the game. What horrifies them is something stranger and harder to explain. It is the horror of watching someone destroy time itself.

Because to a dividend investor, time is not a backdrop. Time is the entire strategy. And day trading, in their eyes, is not just a different approach to the market. It is an attack on the one resource they spent years carefully accumulating.

The Quiet Religion of Compounding

To understand why dividend investors react this way, you have to understand what they actually believe in. And what they believe in is not stocks. It is not even dividends, really. It is compounding.

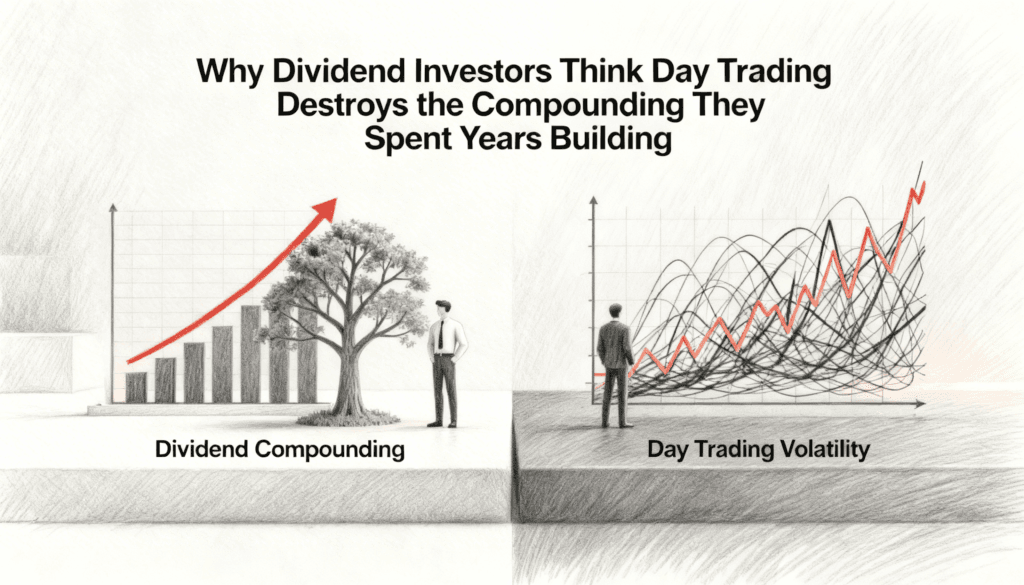

Compounding is the closest thing finance has to a mystical force. The idea is almost embarrassingly simple. You invest money. It earns money. That earned money also earns money. And on and on, for years, until the numbers start doing things that look impossible. A small stream becomes a river. A boring portfolio becomes a small fortune. The math is not complicated. The patience required is.

Dividend investors are the monks of this religion. They do not just believe in compounding. They organize their entire lives around protecting it. They reinvest every payment. They avoid selling. They hold through crashes, through recessions, through years when their strategy looks ridiculous compared to whatever is trending that month. They are playing a game that only makes sense if you zoom out far enough to stop seeing the individual years.

And then they look at a day trader, and they see someone who has not just chosen a different game. They see someone who has chosen to chop down the tree every morning to measure how much it grew overnight.

What Gets Lost When You Move Too Fast

Here is the part that is hard to convey without sounding preachy. Compounding is not just about leaving money alone. It is about leaving decisions alone.

Every time you sell a position, something breaks. You pay taxes on the gains, which means less money is working for you tomorrow. You pay fees, which do the same thing in a smaller way. But more importantly, you reset the clock on the one thing that actually matters. The longer something has been compounding, the more it has already compounded, and the more each additional day is worth. A stock you have held for fifteen years is not the same thing as a stock you have held for fifteen days. It is not just older. It is denser. It carries more weight per unit of time.

Day trading does not just avoid this process. It actively prevents it from ever starting. Every position is closed before it can mature. Every gain is crystallized before it can snowball. The trader might make money, sometimes a lot of money, but the dividend investor watching from the sidelines sees something the trader does not. They see a person who keeps pouring water into a bucket with holes drilled in the bottom and wondering why the bucket never fills.

The irony is that day traders often accuse dividend investors of being passive. But dividend investors would argue the opposite. They would say that doing nothing is the hardest thing in finance. Anyone can click buttons. Very few people can sit still for twenty years while their neighbors get rich and then poor and then rich again chasing the latest thing.

The Gardener and the Chef

There is a metaphor that might help here, even though metaphors in finance are usually overused. Think of a dividend investor as a gardener and a day trader as a chef.

The gardener plants things and waits. They water, they prune, they protect the soil. Their work is mostly invisible, because most of what matters is happening underground. The harvest, when it comes, is the accumulation of years of quiet effort. The gardener is not trying to be clever. They are trying to not ruin what is already growing.

The chef operates on a different timeline entirely. Ingredients come in, meals go out, and the cycle repeats daily. A great chef can make extraordinary things happen in a single evening. But a chef cannot store a meal for twenty years and expect it to become more valuable. The value of their work is in the immediacy of the execution.

Both are skilled. Both can make a living. But if you put a chef in charge of a garden, and tell them to check on it every ten minutes and rearrange the plants based on how they look in the morning light, you will not get a better garden. You will get a dead one.

This is how dividend investors see day trading. Not as wrong, exactly. Just as a completely different activity being confused for the same thing.

The Psychology Nobody Talks About

There is a deeper layer here, and it has more to do with human nature than with finance. The stock market is one of the few places where your worst instincts are rewarded in the short term and punished in the long term. Panic selling feels smart when the market is falling. Buying at the top feels smart when everyone is celebrating. Checking your portfolio every hour feels productive, even though it has been shown, again and again, that the people who check least often tend to do best.

Dividend investors have built a strategy that is essentially a defense mechanism against their own minds. By focusing on the income stream instead of the stock price, they give themselves something to watch that does not move much. Dividends tend to be stable. They usually grow slowly. They rarely get cut without warning. Watching dividends come in is boring in the best possible way. It lets the investor ignore the price chart, which is where most of the bad decisions live.

Day trading does the opposite. It forces the trader to stare directly at the thing most likely to mislead them. Price. Every second. For hours. Trying to outthink a market that is made of millions of other people trying to do the exact same thing. It is not that day traders are dumb. Many are brilliant. It is that the game they have chosen is cognitively brutal in a way that compounding simply is not. The dividend investor wins by removing themselves from the decision. The day trader wins by making more good decisions in a day than most people make in a year.

Why This Debate Feels Personal

You could read all this and think it is just a disagreement about strategy. But anyone who has spent time in these communities knows it is not. It is personal. Dividend investors do not just think day trading is inefficient. They think it is wasteful in a way that offends something in them.

Part of this is aesthetic. There is a certain kind of person who finds beauty in slow, boring, repetitive accumulation. The same person who enjoys long walks, old books, and meals that take hours to prepare. To that person, day trading is not just a different choice. It is a rejection of a worldview. It says that patience is for people who could not figure out how to be fast. And dividend investors, quite reasonably, take this personally.

But there is something else going on too. Dividend investors have made a bet that the future will reward waiting. Every day trader who gets rich quickly is, in some small way, evidence that this bet might be wrong. Or at least that there was an easier path. The dividend investor does not need day traders to fail, exactly. But they need the idea of long term compounding to remain sacred. Otherwise the decade they spent doing nothing starts to look like a decade they wasted.

This is why the arguments get heated. It is not about money. It is about whether a life organized around patience was worth living.

The Part Neither Side Wants to Hear

Here is the uncomfortable truth that closes most debates in finance if you let it.

Dividend investors are right that compounding is one of the most powerful forces in personal wealth. They are right that most day traders lose money. They are right that time in the market matters more than timing the market for almost everyone. These are not opinions. They are closer to facts.

But they are also sometimes wrong about the shape of a good life. Not everyone has forty years. Not everyone has the temperament for slow accumulation. Not everyone finds meaning in doing nothing well. Some people need the feedback loop of daily decisions to feel alive in their own finances. For them, a dividend strategy would not be peaceful. It would be torture.

And day traders, in turn, are sometimes right about dividend investors. Some of them really are just hiding behind a strategy to avoid engaging with the market at all. Some of them have confused stillness with wisdom. Some of them have spent years holding positions they should have sold, telling themselves that any action would disturb the sacred process of compounding.

The truth, as usual, is that compounding is not a moral category. It is just math. The question is not whether you believe in it. The question is whether the life you want can actually be built on top of it. For most people, the answer is yes. For some, the answer is no. And the loudest arguments in this debate usually come from people who have not yet figured out which group they belong to.

The dividend investor watches the day trader and sees destruction. The day trader watches the dividend investor and sees stagnation. They are both looking at the same market. They are both, in a sense, looking at the same mirror. And what they see reflected back is mostly themselves.