Table of Contents

The Dinner Party Wince That Tells You Everything About Modern Investing

There is a moment at every dinner party in 2026 when someone mentions Warren Buffett, and a younger guest at the table physically winces. It is not because they dislike the man. They have never met him. They wince because invoking Buffett today feels a little like quoting your grandfather for dating advice. The wisdom may be perfectly sound, but the cultural distance feels enormous.

Value investing, the philosophy Buffett did not invent but certainly turned into a global religion, finds itself in an awkward position. This is the discipline that built dynasties, funded universities, and produced more billionaires per capita than any other investment style in modern financial history. And yet, if you ask a twenty six year old with a brokerage app what they think about buying boring companies at sensible prices, you will get a polite nod followed by a swift change of subject toward something involving artificial intelligence chips or a digital coin named after a meme.

So the question deserves an honest hearing. Is value investing genuinely outdated, the financial equivalent of a flip phone in a smartphone world? Or is it simply unfashionable in a way that has happened many times before, only to come roaring back the moment the music stops? To answer that fairly, we need to stop treating value investing as a strategy and start treating it as a worldview. Because that is what it actually is.

The Philosophy Hiding Inside the Spreadsheet

Most people assume value investing is about numbers. Price to earnings ratios. Book value. Discounted cash flow models. The kind of vocabulary that makes eyelids heavy and turns finance into accounting with extra steps. But the numbers are the costume, not the body underneath.

At its core, value investing makes a philosophical claim about how the world works. The claim goes something like this. Markets are made of humans. Humans become scared and greedy in predictable patterns. The price of something and the worth of something are two separate things that occasionally meet by accident. Patience, applied carefully, tends to be rewarded. Hype, applied generously, tends to be punished.

If you strip away the jargon, that is essentially Stoicism with a brokerage account. It is the Marcus Aurelius approach to capital. Do not get excited. Do not get sad. Notice what is durable. Ignore what is loud. Wait.

Value investing was never really a method for finding cheap stocks. It was a method for staying sane while everyone around you loses their composure.

This is also exactly why the discipline feels so out of step with the current moment. We do not live in a culture that rewards waiting. We live in a culture that rewards announcing. The dopamine economy has rewired what investing even looks like to a new generation. Investing has become something you do in public, in real time, with screenshots attached. Value investing, by contrast, is mostly something you do alone, slowly, and with the lights off.

Why the Mindset Matters More Than the Metrics

When you understand value investing as a temperament rather than a toolkit, the entire debate changes. The metrics were always servants to a deeper idea. They existed to enforce discipline on people who would otherwise be swept away by their own emotions. A low price to earnings ratio is just a guardrail. The real skill is the willingness to act calmly when the crowd is screaming.

That distinction matters because it explains why the philosophy survives even when specific formulas stop working. Formulas age. Human psychology does not. The fear that gripped investors in 1929 is the same fear that gripped them in 2008 and in March of 2020. The names changed. The feeling did not.

The Generational Optics Problem

There is a clear reason value investing has become a punchline, and it has nothing to do with the math breaking down. It is because the storytelling stopped working.

Consider how the average person under thirty actually encounters investing today. They open an app. They see a chart. The chart climbs dramatically or it collapses dramatically. There is a comment section. There are memes. There is a community of strangers all pretending they know exactly what happens next. The entire experience is engineered to feel like a sport with live commentary.

Now imagine trying to insert a strategy into that environment whose central pitch is, roughly, “buy a company that manufactures industrial paint, then do absolutely nothing for eleven years.” The strategy is not wrong. The strategy is unwatchable. There is no narrative arc. There is no villain to defeat. There is no screenshot worth sharing. The returns may eventually be excellent, but you cannot stream the process on TikTok.

This is the genuine weakness value investing carries today. It is not intellectually obsolete. It is dramatically inert. And in an attention economy, being boring sits much closer to being dead than to being respectable. The discipline did not lose its edge. It lost its audience.

The Cost of Confusing Entertainment With Returns

Here is the quiet danger nobody warns young investors about. The strategies that feel the most exciting are very often the ones that perform the worst over a full lifetime. Constant trading generates fees, taxes, and emotional exhaustion. The companies with the loudest fan bases are frequently the most overvalued. Entertainment and compounding pull in opposite directions more often than people realize.

A strategy that bores you to tears might be the very thing that retires you early. That is an uncomfortable truth in a world that has trained an entire generation to associate engagement with quality.

What the Critics Actually Get Right

The world has changed in ways that genuinely complicate traditional value frameworks, and any defender of the philosophy who refuses to admit this is simply not paying attention.

A growing share of corporate value now lives in things that never appear cleanly on a balance sheet. Brand power. Network effects. Software that improves itself over time. Talented engineers who can walk out the door whenever they choose. These are real sources of worth, and the classical value metrics struggle to capture any of them. A company can look expensive by every traditional measure and still be deeply undervalued if its competitive position widens with every passing quarter.

Then there is the matter of speed. Information used to move slowly. A patient investor could uncover a mispriced stock simply because most people had not bothered to read the annual report. Today, every annual report gets read within minutes, dissected by algorithms, and priced in minutes or hours. The easy inefficiencies have mostly been competed away.

The old advantage of value investing was finding what others ignored. The new advantage is doing what others cannot bring themselves to do.

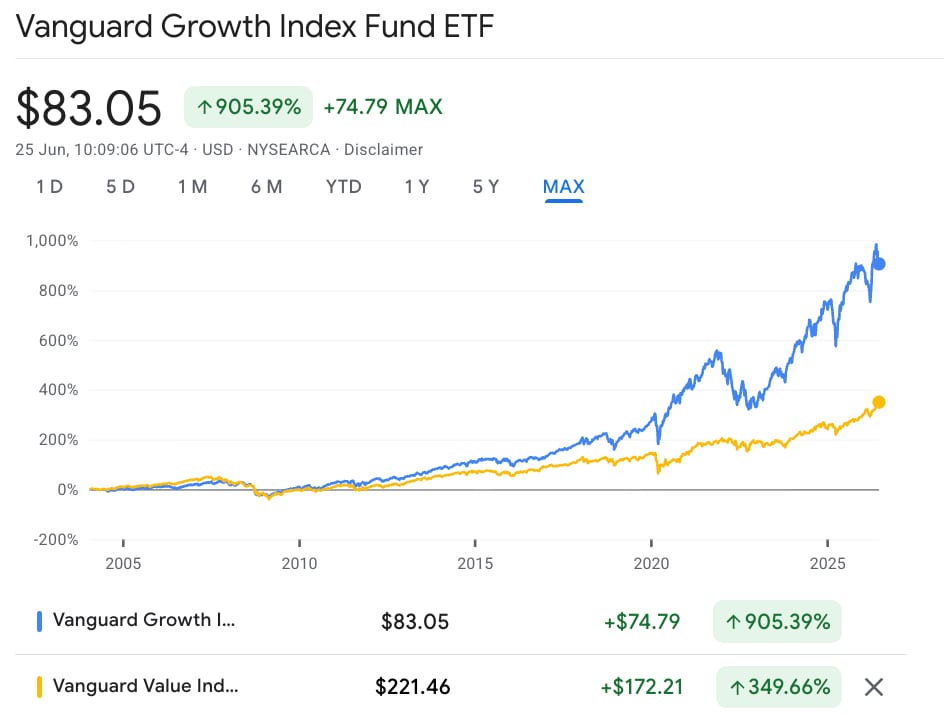

And then there is the elephant standing in the corner of the room. For long stretches of recent history, growth has simply beaten value. Not by a little. By a great deal.

You can argue this is a temporary anomaly that will eventually revert. You can argue it reflects structural changes that will persist for decades. But you cannot argue with the scoreboard. An entire generation entered the market during a period when patience with cheap stocks was punished and enthusiasm for expensive ones was lavishly rewarded. That experience shapes how those investors interpret everything that follows.

The Part Both Sides Miss

This is where the conversation becomes genuinely interesting, and slightly uncomfortable for everyone involved.

The most aggressive critics of value investing love to point at the past fifteen years, during which a handful of technology companies obliterated nearly every traditional valuation framework anyone tried to apply to them. If you bought Amazon when it looked outrageously expensive, you became wealthy. If you avoided Tesla because the numbers refused to cooperate, you missed one of the great wealth creation stories of the era. The lesson appeared obvious. The old rules were broken beyond repair.

But there is a quieter lesson buried inside that exact same period, and almost nobody talks about it. The people who actually captured the most money from those companies were not the ones constantly trading in and out of them. They were the people who bought and then held. For years. Through terrifying drawdowns and breathless rallies alike.

In other words, the most successful growth investors of the modern era behaved almost exactly like value investors in their temperament, even when their spreadsheets looked entirely different. They were patient. They tolerated boredom. They ignored the noise. They believed in the long term worth of a business they understood, and they refused to sell simply because someone on television had a feeling about interest rates.

That is value investing wearing a different outfit. The clothes changed. The discipline survived intact.

One Flavor Aged, Not the Whole Tradition

So when commentators declare value investing dead, what they usually mean is that one specific flavor of it, the kind obsessed with cheap industrial companies trading below book value, has endured a brutal stretch. That observation is fair. But conflating that narrow flavor with the entire philosophy is a bit like declaring that reading is dead because nobody buys printed encyclopedias anymore. The format aged. The activity did not.

The investors who understood this never panicked. They simply updated their lens. They recognized that durable competitive advantage is a form of value, even when it carries a premium price tag. They applied the timeless temperament to a changed economy, and they prospered while purists and gamblers both struggled.

The Real Question We Should Be Asking

Perhaps the smarter approach is to stop arguing about whether value investing is dead and start asking what it was truly teaching us in the first place.

If you actually read the original texts, the Benjamin Graham books that started the whole tradition, you discover something surprising. Graham was not really obsessed with cheap stocks. He was obsessed with not being a fool. His central message was that the market behaves like a manic and depressive business partner who will offer you wildly different prices for the very same thing depending entirely on his mood, and that your job is to remain the calm one in the relationship.

That is not a stock picking technique. That is a character trait dressed up in financial language.

Graham did not teach people how to value companies so much as he taught them how to value their own composure. The numbers were simply the discipline that protected investors from themselves.

Seen this way, value investing was always about temperament first and mathematics second. The ratios and formulas were tools to enforce restraint on people who would otherwise be carried off by their own emotions. The entire apparatus existed to protect investors from the most dangerous variable in any portfolio, which is the human being who owns it.

Where the Dismissive Framing Falls Apart

Here is where the casual “that is just old fashioned thinking” framing begins to crumble. If the past few years revealed anything, it is that most people, regardless of their age, struggle desperately with their own emotions the instant money is involved.

Watch how quickly confident traders dissolve into panic during a sharp downturn. Watch how easily a committed pessimist flips to wild optimism after three good weeks. The technology changed. The brokerage interface became sleeker. The psychology underneath remained precisely as fragile as it was when Graham sat down to write in the middle of the last century.

Which means the insight value investing was secretly teaching all along, the discipline of not flinching, of separating noise from signal, of accepting that on most days nothing important actually happens, has become more valuable rather than less. The faster the world moves, the greater the edge belongs to the mind that refuses to move with it.

So Is Value Investing Actually Outdated?

The most honest answer is that the brand is outdated. The substance is not.

Value investing in its purest and most rigid form, the version obsessed with industrial conglomerates and discarded cigar butt stocks trading for pennies on the dollar, will probably continue to feel old fashioned. The economy itself has shifted toward things that no longer resemble industrial conglomerates. That is completely fine. Strategies are allowed to age. Specific tactics are allowed to retire gracefully.

But the underlying mindset is a different matter entirely. The willingness to think for yourself. The discipline to wait when waiting is wildly unpopular. The nerve to buy when others are dumping everything they own. The patience to do nothing while the crowd loses its mind. That mindset is a permanent competitive advantage, and it works for a reason that has nothing to do with cleverness. It works because almost nobody can actually do it.

The Most Expensive Joke a Young Investor Can Tell

So calling value investing the embarrassing relic of finance might turn out to be the most expensive joke a young investor ever tells. The aesthetic genuinely has aged. The vocabulary sounds dated. The spokesman is in his nineties. All of that is true.

But dismissing the philosophy underneath the aesthetic means surrendering the one edge that has survived every market crash, every technological revolution, and every generation that came before this one. The discipline does not care whether you find it stylish. It simply compounds in silence while louder strategies burn out.

What This Means for the Way You Invest Today

You do not need to buy industrial paint companies to honor what value investing was teaching. You need to internalize three habits that translate across any era.

First, separate the price of an asset from its actual worth, because the market will constantly confuse the two for you. Second, build a temperament that treats volatility as opportunity rather than threat. Third, accept that the most powerful investing decisions usually feel like doing nothing at all.

Apply those three principles to whatever the modern economy produces, whether that is software, semiconductors, renewable infrastructure, or businesses that have not been invented yet, and you are practicing value investing in its truest sense. The labels do not matter. The discipline does.

The previous generation may have had questionable taste in music and even worse taste in neckties. Their investing instincts, it turns out, were not the worst part of the package. They were the part most worth keeping.