Table of Contents

Let me start with a scene you already know.

You are at a restaurant. The bill arrives. There is a 3% surcharge for using a credit card. It amounts to maybe $1.80 on your meal. And something inside you tightens. You feel it in your chest. A tiny flare of injustice. You consider paying cash. You might even mention it to the person sitting across from you. “Can you believe they charge for that?”

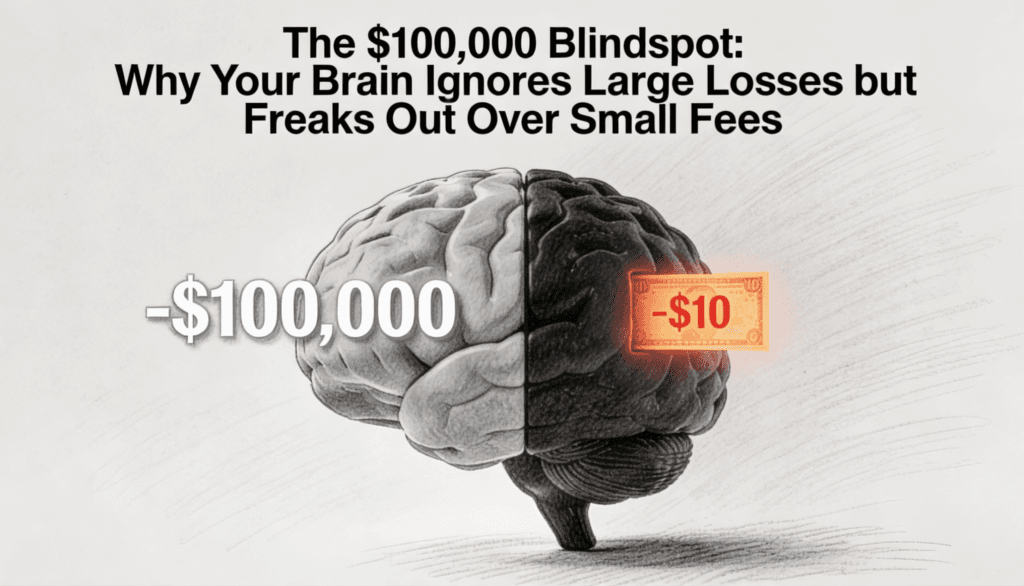

Now rewind to earlier that same week. Your investment portfolio dropped $100,000 in a single afternoon. You glanced at your phone, registered the number, and went back to whatever you were doing. Maybe you shrugged. Maybe you did not even shrug.

$1.80 got a reaction. $100,000 got nothing.

This is not a quirk. This is architecture. Your brain was built this way on purpose, and understanding why is one of the most valuable things you can do with the next few minutes.

The ancient math your brain still runs on

Your nervous system did not evolve to manage a brokerage account. It evolved to manage a calorie budget. For most of human history, the things that could hurt you were immediate, concrete, and close enough to touch. A rival takes food from your hand. A predator steps on a branch behind you. Someone cheats you in a trade.

These threats shared a pattern. They were specific, visible, and personal. Your brain built an alarm system calibrated to exactly this kind of loss.

But a portfolio declining? That is abstract. It is numbers on a screen changing color. There is no rival standing in front of you. There is no branch snapping. The loss is real, often enormous, but it arrives in a format your alarm system was never trained to detect.

So the fee at the restaurant triggers your ancient wiring. The portfolio loss floats past it.

Think of it this way. Your brain is a smoke detector that was designed for campfires. It goes off when someone lights a match in the next room. But somehow it stays silent when the entire forest behind your house is burning. The match is the surcharge. The forest is your net worth.

Why small feels big and big feels nothing

The researcher Paul Slovic documented this pattern while studying how people respond to humanitarian crises. He found that people feel the most empathy for a single identified victim. Show them one child with a name and a photograph, and they open their wallets. Show them a statistic about 500,000 people suffering, and they feel almost nothing. The emotion does not scale with the number. It often inverts.

The same machinery runs your financial brain. One overdraft fee of $35 will irritate you for a week. A slow bleed of $40,000 in a sideways market over eighteen months will barely register as a memory. The $35 is sharp, specific, and feels like someone did it to you. The $40,000 is diffuse, gradual, and feels like weather.

This creates a brutal irony. The losses most likely to ruin you financially are the exact losses your brain is least equipped to care about.

The visibility tax

There is another layer here, and it has to do with something I call the visibility tax. We do not respond to the size of a cost. We respond to how visible it is.

A $4 ATM fee is extremely visible. It appears on your screen with a yes or no choice. It practically begs you to be outraged. And many people will walk three blocks to avoid it.

Meanwhile, the expense ratio on a mutual fund might be quietly siphoning tens of thousands of dollars from your returns over a decade. But that cost never shows up as a line item you have to approve. It is silently deducted. No notification. No confirmation screen. No moment of choice.

The ATM fee is a mosquito. It is annoying, you can see it, and you swat at it. The expense ratio is carbon monoxide. Odorless. Invisible. And potentially far more dangerous.

This is not an accident of financial product design. It is the product design. The industry learned long ago that people do not fight costs they cannot see. So the most profitable fees are the ones that never trigger a moment of conscious decision. They exist below the threshold of your attention, which is exactly where they do the most damage.

The strange case of active attention

Here is where it gets interesting. Paying more attention to your investments does not fix this problem. In many cases, it makes it worse.

Behavioral finance research has consistently shown that investors who check their portfolios more frequently tend to take on more risk and earn lower returns over time. This is because frequent checking exposes you to more of those small, visible losses. Each red day triggers a micro dose of that ancient alarm system. Over time, these micro doses accumulate into a general sense of anxiety that pushes you toward overly conservative choices.

So the investors who watch closely get punished by their own attention. And the investors who ignore their portfolios often do better precisely because their neglect protects them from the distortion.

This is the financial equivalent of a doctor telling you that the best thing you can do for your health is to stop checking your symptoms online every night. Sometimes the cure for bad pattern recognition is less data, not more.

What this means for real decisions

Let me bring this out of the abstract and into the room where you actually make choices.

You probably spend mental energy optimizing for small visible costs. Canceling a $12 subscription. Switching banks over a $5 monthly maintenance fee. Driving to the cheaper gas station. Clipping coupons, literal or digital. None of these are irrational moves on their own, but they become a problem when they eat up all the attention you have for financial decisions while the big invisible costs go unexamined.

The rebalancing you did not do because the portfolio looked “fine.” The insurance policy you never compared because the premium comes out automatically. The house you held onto two years too long because selling felt like a specific, visible action while holding felt like doing nothing.

Doing nothing always feels free. It almost never is.

The asymmetry of regret

We do not just feel small losses more intensely in the moment. We also remember them more specifically.

Ask someone about their financial regrets and they will almost always point to a specific, concrete decision. “I sold that stock too early.” “I bought that car.” “I paid that contractor too much.” These are vivid, retrievable memories because they were tied to a specific action and a visible outcome.

But ask them about the cost of their general inertia over the past decade and you will get a blank look. Nobody lies awake regretting the vague slow erosion of returns from a mediocre asset allocation. There is no scene to replay. No villain. No moment of decision. Just a long, featureless stretch of slightly less wealth than they could have had.

The regrets that keep us up at night are almost never the ones that cost us the most.

Every financial product, every market cycle, and every year of inertia carries a cost. Some of those costs are printed on a receipt and designed to make you flinch. Others are buried in the architecture of your defaults and designed to be invisible.

The $1.80 surcharge at the restaurant is not your problem. It never was. Your problem is the quiet, enormous, slow moving number that your perfectly functioning ancient brain has decided is not worth worrying about.

The smoke detector works fine. It just was not built for this kind of fire.